Introduction: Best Mutual Fund for Beginners with Low Risk

Starting your investment journey can feel overwhelming, especially when you’re worried about losing money you’ve worked hard to save. If you’ve ever opened an investing app, stared at hundreds of fund names, and closed it without investing a single rupee — you’re not alone. Most beginners aren’t looking for the fund that will make them rich overnight.if you’re still building your financial basics, it’s worth starting there first. They’re looking for something safer: a way to grow their money steadily, without watching it crash 20% in a bad month.

The good news is that mutual funds aren’t a single “high-risk, high-reward” product. They’re a spectrum. On one end you have volatile small-cap equity funds; on the other, you have debt funds that behave almost like a smarter fixed deposit. Somewhere in between sits a sweet spot for beginners — funds that offer capital stability, modest but consistent growth, and low emotional stress.

In this guide, we’ll break down exactly what “low risk” means in the mutual fund world, walk through the fund categories best suited to beginners, show you real numbers (not just vague percentages), and give you a step-by-step path to actually opening your first investment — not just understanding the theory.

What Is a Mutual Fund?

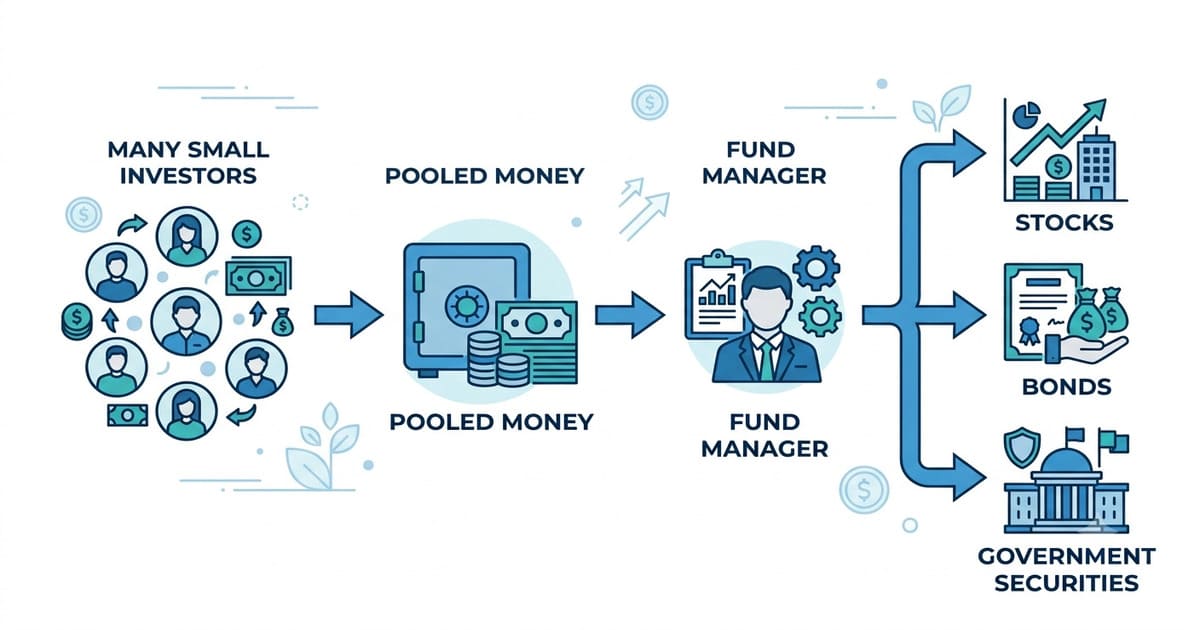

A mutual fund is an investment vehicle that pools money from thousands of investors and invests it collectively in assets such as:

- Stocks (equity)

- Government and corporate bonds (debt)

- Government securities (G-Secs)

- Money market instruments (treasury bills, commercial paper)

A professional fund manager, backed by a research team, decides where this pooled money goes, based on the fund’s stated objective. You don’t need to track individual companies or bond issuers — you own a small

slice of a large, professionally managed basket. ( For a deeper breakdown of how mutual funds work, our dedicated guide covers the fund structure in more detail.)

Every mutual fund in India is regulated by the Securities and Exchange Board of India (SEBI), which mandates strict disclosure norms, including a standardized Riskometer on every scheme (more on this below) and mandatory scheme information documents.

Why Mutual Funds Are Ideal for Beginners

- Diversification reduces risk — your money is spread across dozens or hundreds of securities instead of riding on one stock.

- Professional management — a qualified fund manager and research team make the calls.

- Low entry barrier — you can start with as little as ₹100–₹500 through an SIP.

- Easy automation — SIP lets you invest on autopilot every month.

- No market expertise required — you don’t need to read balance sheets or track interest rate cycles yourself.

- Regulatory oversight — SEBI regulation means standardized disclosures, audited NAVs, and investor protection mechanisms that individual stock investing doesn’t offer.

👉 This combination — professional management plus low minimums — makes mutual funds one of the most accessible starting points for new investors in India.

What Does “Low Risk” Actually Mean in Mutual Funds?

This is where most beginners get confused. Low risk does not mean zero risk or guaranteed returns. Unlike a bank fixed deposit, no mutual fund promises a fixed return, because the underlying assets are market-linked.

“Low risk” in the mutual fund context means:

- A lower probability of significant capital loss over a short period

- Lower volatility — the fund’s value doesn’t swing wildly month to month

- More predictable, if modest, returns compared to pure equity funds

- Underlying investments in relatively safer instruments (government securities, high-credit-rated corporate bonds)

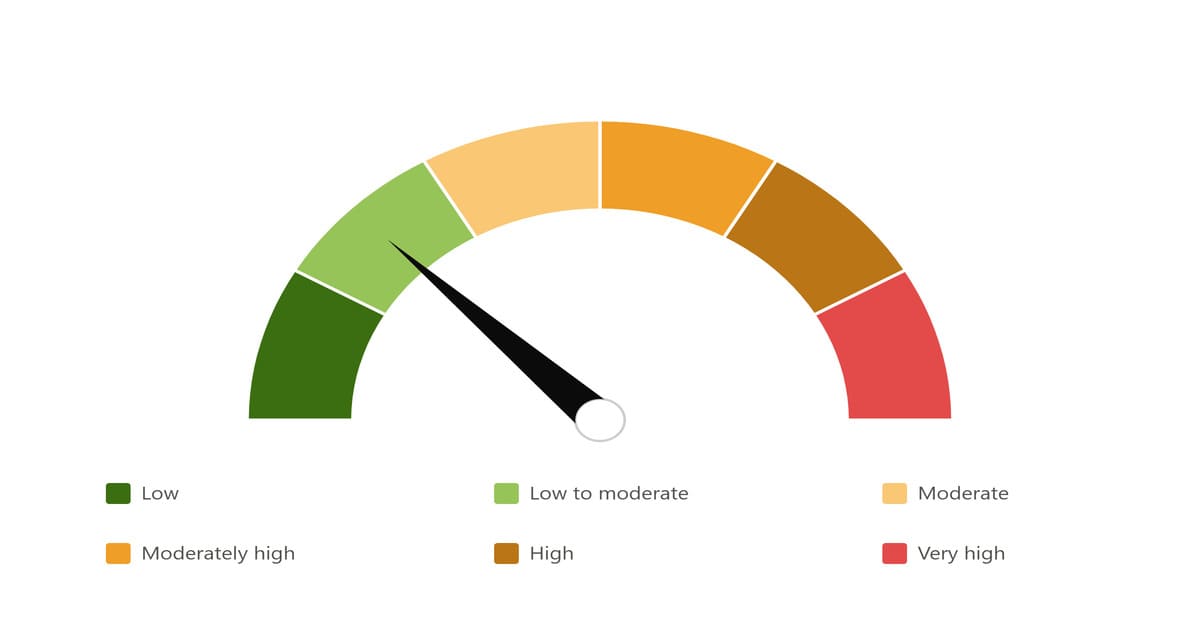

Understanding the SEBI Riskometer

Every mutual fund scheme in India displays a Riskometer — a mandatory, standardized visual gauge with six levels:

- Low

- Low to Moderate

- Moderate

- Moderately High

- High

- Very High

Before investing in any fund, check its current Riskometer rating on the fund factsheet or the AMC’s website, following SEBI’s official Riskometer guidelines.

Low-Risk Mutual Funds Typically Invest In:

- Government bonds and treasury bills (sovereign guarantee, near-zero default risk)

- High-rated corporate bonds (AAA-rated issuers)

- Fixed-income and money market instruments

- Balanced portfolios that blend a small equity component with a larger debt component

👉 These funds are built around capital protection first, steady growth second — the opposite priority order of an aggressive equity fund.

Best Types of Mutual Funds for Beginners with Low Risk

Instead of chasing specific scheme names — which change performance rankings every quarter — it’s far more useful to understand the categories. Category-level understanding stays relevant for years; scheme rankings don’t.

1️⃣ Debt Mutual Funds

Debt mutual funds invest in fixed-income instruments like government securities, corporate bonds, and treasury bills. Within “debt funds,” there’s actually a sub-spectrum worth knowing:

| Sub-Category | Typical Holding Period | Best For |

|---|---|---|

| Liquid Funds | Up to 91 days | Parking emergency funds, better than a savings account |

| Ultra-Short Duration Funds | 3–6 months | Short-term goals, slightly better returns than liquid funds |

| Short Duration Funds | 1–3 years | Medium-term goals with modest interest-rate risk |

| Corporate Bond Funds | 2–4 years | Investors wanting quality (mostly AAA-rated) corporate exposure |

Best For:

- Conservative investors who prioritize capital safety

- Short- to medium-term financial goals (1–3 years)

- Investors who want predictable, bond-like returns

Expected Returns:

Roughly 6%–8% annually, though this fluctuates with prevailing interest rates —and if you’re weighing this against a more familiar option, see how SIP compares to a recurring deposit before deciding where your money should go.

Risk Level:

- Low to moderate (interest rate risk and credit risk exist, but are limited compared to equity)

Why Beginners Should Consider Debt Funds

- Meaningfully lower volatility than equity funds

- A better place to park money than letting it sit idle in a savings account

- Useful as a “starter fund” before beginners get comfortable with market-linked investing

- Can act as the safety anchor in a beginner’s overall portfolio

2️⃣ Balanced Advantage Funds (Dynamic Asset Allocation Funds)

Balanced Advantage Funds (BAFs) automatically shift the portfolio’s equity-to-debt ratio depending on market valuations — increasing debt exposure when markets look expensive, and increasing equity exposure when markets look cheap. This built-in, model-driven rebalancing is exactly the discipline most beginners struggle to do on their own.

Best For:

- Beginners who want growth potential and a safety net, without managing the split themselves

- Long-term wealth creation (5+ years)

- Investors who get anxious watching pure-equity fund NAVs swing

Expected Returns:

- Roughly 8%–12% annualized over the long term (varies with market cycles)

Risk Level:

- Moderate, but actively controlled by the fund’s internal allocation model

👉 Because they blend growth and safety in a single product, Balanced Advantage Funds are often considered the best all-round category for beginners with low-to-moderate risk appetite.

A close cousin worth knowing: Conservative Hybrid Funds, which hold roughly 75–90% debt and only 10–25% equity — an even gentler entry point than a standard BAF, ideal for extremely risk-averse first-time investors.

3️⃣ Index Funds (Large Cap)

Index funds simply replicate a market index — most commonly the Nifty 50 or Sensex — by holding the same stocks in the same proportion as the index. There’s no active stock-picking involved.

Best For:

- Long-term investors (7+ years) comfortable with equity market ups and downs

- Passive investors who prefer a “set and forget” approach

- Beginners who want simplicity and full transparency in what they own

Risk Level:

- Moderate to moderately high (it’s still equity, so short-term volatility is real)

Why They’re Considered Safer Than Other Equity Funds

- Exposure only to large, established, financially stronger companies

- No “fund manager risk” — the fund can’t underperform the index by picking bad stocks, since it isn’t picking at all

- Typically the lowest expense ratio in the equity category, meaning more of your return stays with you

👉 Index funds provide long-term growth with meaningfully lower risk than mid-cap or small-cap funds — but they are still equity, so they belong in a beginner’s portfolio only alongside a debt or hybrid cushion, not as the sole holding.

Quick Comparison: Which Category Fits You?

| Fund Type | Risk Level | Ideal Time Horizon | Typical Long-Term Return | Best Use Case |

|---|---|---|---|---|

| Liquid/Debt Funds | Low | 3 months – 3 years | 6%–8% | Emergency fund, short-term goals |

| Conservative Hybrid | Low–Moderate | 2–4 years | 7%–10% | First step beyond FD |

| Balanced Advantage Fund | Moderate | 5+ years | 8%–12% | Core beginner portfolio |

| Index Fund (Large Cap) | Moderate–High | 7+ years | 10%–12% | Long-term wealth building |

Should Beginners Start with SIP?

Yes — a Systematic Investment Plan (SIP) is, for most beginners, the smartest way to start, and here’s why with actual numbers instead of just a claim.

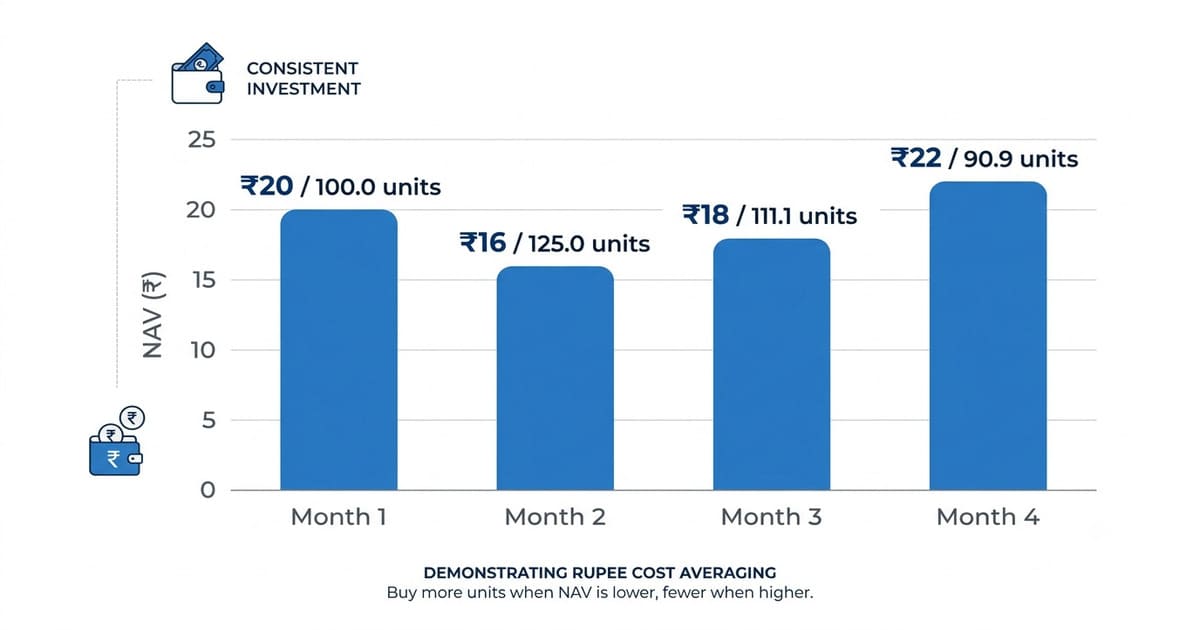

A Real Example: Rupee Cost Averaging in Action

Imagine you invest ₹2,000 every month into a fund whose NAV (price per unit) moves like this over four months:

| Month | NAV (₹) | Units Bought (₹2,000 ÷ NAV) |

|---|---|---|

| Month 1 | ₹20 | 100.0 units |

| Month 2 | ₹16 | 125.0 units |

| Month 3 | ₹18 | 111.1 units |

| Month 4 | ₹22 | 90.9 units |

Total invested: ₹8,000. Total units bought: 427 units. Your average cost per unit works out to roughly ₹18.7- lower than the simple average NAV of ₹19, because you automatically bought more units when prices dipped. If you want to see compounding applied with more real-number examples, that’s where SIP’s long-term power really shows up.

Benefits of SIP

- ✔ Reduces market timing risk — you’re not betting on a single entry point

- ✔ Builds disciplined, automated investing habits

- ✔ Harnesses the power of compounding over time

- ✔ Extremely affordable entry point — start with ₹500–₹1,000 per month

- ✔ Easy to increase gradually via “SIP top-up” or “step-up SIP” features most platforms now offer

👉 SIP isn’t just a payment method — it’s a behavioral tool that protects beginners from their own worst instinct: trying to time the market. That consistency is also why disciplined SIP investing builds long-term wealth even when markets feel uncertain.

How to Choose the Best Mutual Fund for Beginners with Low Risk

Before investing, run every fund through this checklist:

✔ Fund Category First

Start with debt or balanced advantage funds. Add index funds gradually as your comfort with volatility grows.

✔ Expense Ratio

This is the annual fee the fund charges, deducted directly from your returns. A lower expense ratio compounds into a meaningfully larger corpus over 10–15 years. Index funds typically carry the lowest expense ratios in the equity space; actively managed debt and hybrid funds vary more, so compare within the same category.

✔ Fund Performance — Consistency Over Peaks

Look at 3-year and 5-year rolling returns, not just a single standout year. A fund that has stayed in the top half of its category consistently is generally a better sign than one with a single spectacular year followed by underperformance.

✔ Fund House (AMC) Reputation and Track Record

Established, well-regulated Asset Management Companies with long track records and strong risk-management processes tend to be a safer starting point for beginners than newer or niche fund houses.

✔ Credit Quality (for Debt Funds Specifically)

Check the portfolio’s credit rating breakdown — a debt fund holding mostly AAA-rated instruments carries meaningfully lower default risk. You can review AMFI’s classification of debt fund categories for the full breakdown.

✔ Investment Goal and Time Horizon

- Short-term (under 2 years) → Debt or liquid funds

- Medium-term (2–5 years) → Conservative hybrid or balanced advantage funds

- Long-term (5+ years) → Balanced advantage or index funds

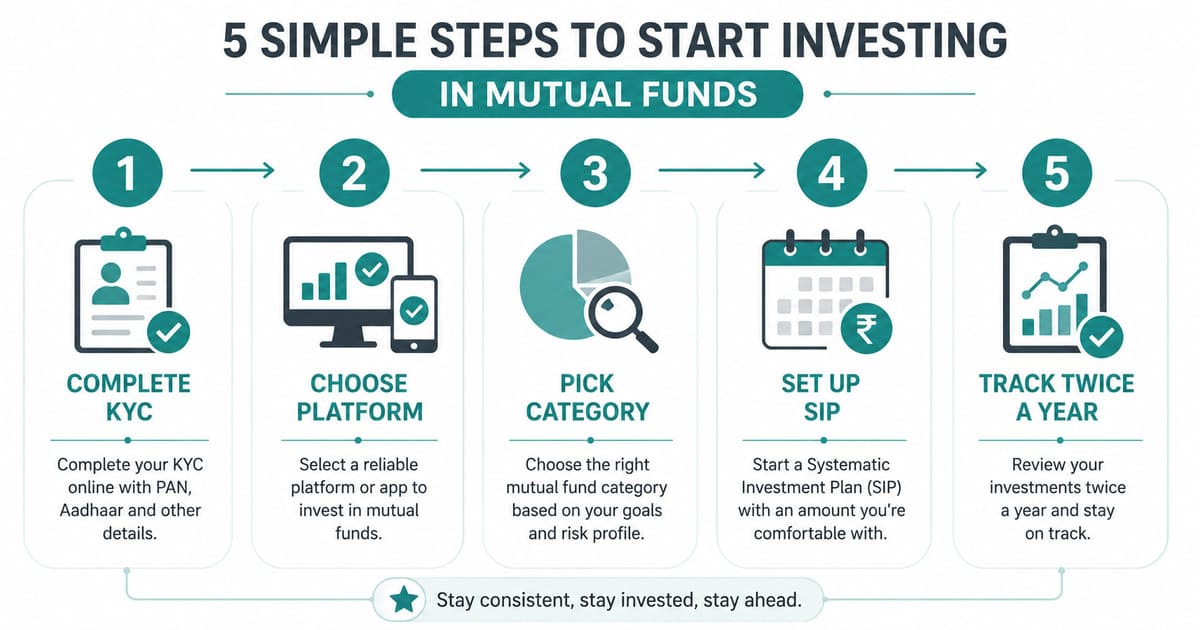

How to Actually Start Investing: A Step-by-Step Walkthrough

Understanding the theory is only half the job. Here’s the practical path:

- Complete your KYC (Know Your Customer). This is mandatory and one-time — done via PAN, Aadhaar, and a simple video verification through any AMC website, registrar (CAMS/KFintech), or investing app.

- Choose a platform. You can invest directly through an AMC’s own website/app (zero distribution commission, called “Direct Plans”) or through an aggregator app/broker (which may offer “Regular Plans” with a small trail commission built in). For beginners, Direct Plans carry a lower expense ratio and are worth the small extra effort to set up.

- Pick your category based on the checklist above, not by asking “which fund is best” on a forum.

- Set up your SIP — decide the amount, the monthly date, and link your bank account for auto-debit.

- Track twice a year, not daily. Checking your NAV every day only amplifies anxiety over short-term noise that doesn’t reflect your long-term outcome.

How Much Should Beginners Invest?

If you’re just starting out:

- Begin with ₹1,000–₹5,000 per month, whatever fits comfortably into your budget

- Increase the amount gradually as your income grows (a “step-up SIP” of even 10% per year makes a large difference over a decade)

- Never invest your emergency fund — keep 3–6 months of expenses in a liquid fund or savings account first, completely separate from your growth investments

👉 The golden rule: invest only surplus money you won’t need in the short term.

Common Mistakes Beginners Should Avoid

- ❌ Chasing last year’s highest returns — past performance doesn’t guarantee future results, and today’s chart-topper is often tomorrow’s laggard

- ❌ Investing without understanding what you own — know whether your money is in debt, equity, or a blend

- ❌ Stopping SIPs during market falls — this is precisely when rupee cost averaging works hardest in your favor

- ❌ Putting all your money into a single fund — even within “low risk,” some diversification across categories helps

- ❌ Expecting quick profits — mutual funds, even low-risk ones, are built for medium-to-long-term goals, not short-term speculation

- ❌ Ignoring the exit load and lock-in period — some funds charge a fee if you withdraw within a specified period (commonly 1 year); always check before investing

👉 Remember: consistency beats timing the market, almost every time.

Realistic Return Expectations

Mutual funds are market-linked investments — there is no guaranteed number. But here’s a realistic long-term range based on historical category averages:

Expected Long-Term Returns (Illustrative, Not Guaranteed):

- Debt Funds: 6%–8%

- Conservative Hybrid Funds: 7%–10%

- Balanced Advantage Funds: 8%–12%

- Index Funds: 10%–12%

What This Looks Like Over Time

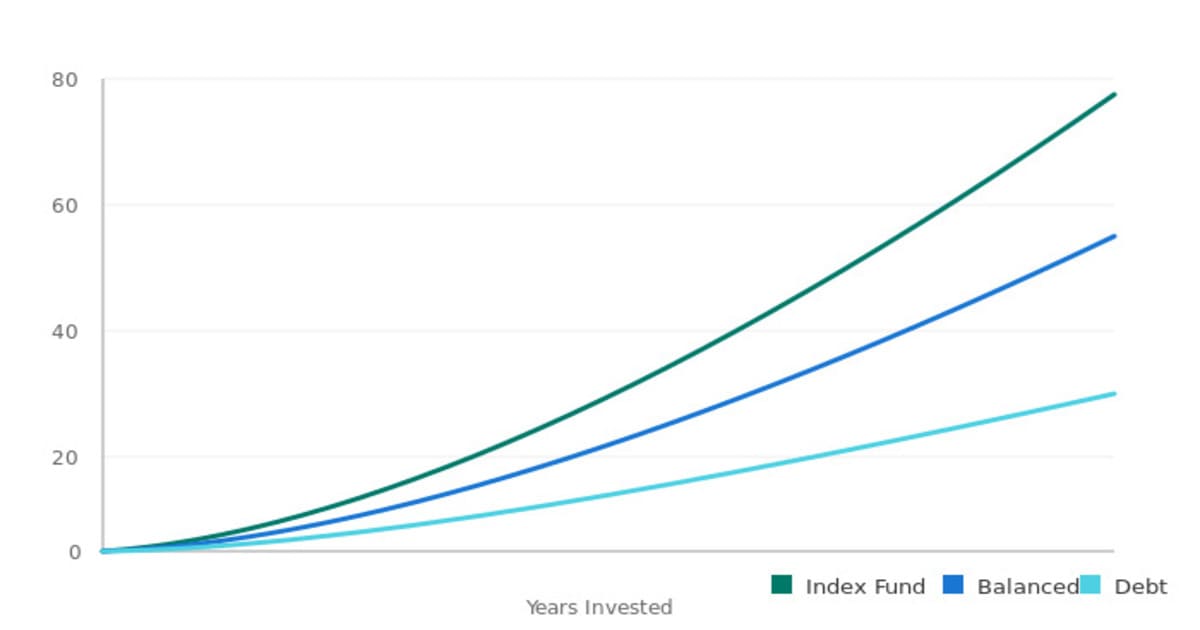

A ₹5,000 monthly SIP, compounded annually (illustrative, ignoring taxes and expense ratio for simplicity):

| Fund Category | Assumed Return | Value After 10 Years | Value After 20 Years |

|---|---|---|---|

| Debt Fund | 7% | ~₹8.7 lakh | ~₹26.3 lakh |

| Balanced Advantage | 10% | ~₹10.3 lakh | ~₹38.3 lakh |

| Index Fund | 11% | ~₹11 lakh | ~₹43.9 lakh |

(These are illustrative projections based on assumed constant returns; actual mutual fund returns fluctuate year to year and are never guaranteed.)

👉 The gap between categories widens dramatically over longer horizons — which is exactly why time in the market, not just fund choice, is a beginner’s biggest asset.

Taxation of Mutual Funds: What Beginners Need to Know

Tax treatment is one of the most overlooked factors when beginners compare fund options — and it directly affects your actual take-home return.

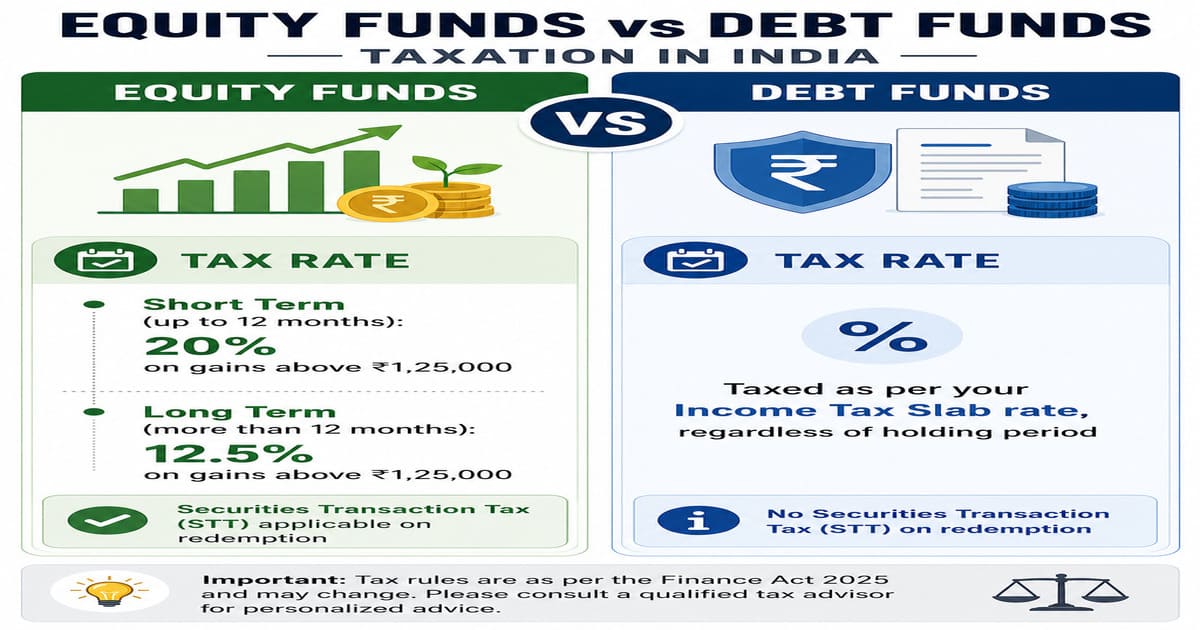

- Equity-oriented funds (including index funds and equity-heavy hybrid funds) held for more than 12 months are taxed as Long-Term Capital Gains (LTCG). Held for less than 12 months, gains are taxed as Short-Term Capital Gains (STCG) at a higher rate.

- Debt funds are taxed based on your applicable income tax slab rate, regardless of the holding period, under rules that took effect from April 2023 onward.

- Balanced Advantage / hybrid funds are taxed as equity or debt depending on their actual equity allocation, which can shift the tax treatment — check the specific fund’s equity allocation policy.

Because tax rules are revised periodically in the Union Budget, always verify current LTCG/STCG rules on the Income Tax Department’s website or with a qualified tax advisor before making decisions based on tax efficiency.

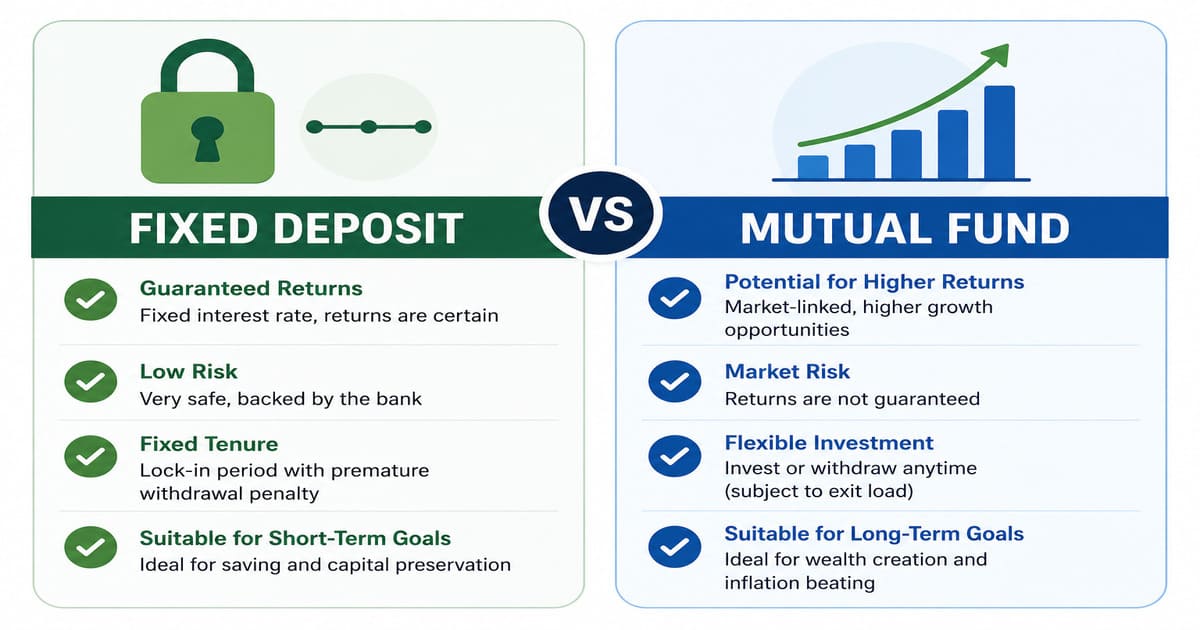

Mutual Fund vs Fixed Deposit (FD)

Many beginners compare mutual funds with the more familiar fixed deposit. Here’s an honest side-by-side:

Fixed Deposits (FD)

- Safe and contractually guaranteed returns

- Lower returns, typically 5%–7%

- No market-linked risk, but interest is fully taxable at your slab rate

- Premature withdrawal usually comes with a penalty

Mutual Funds (Low-Risk Categories)

- Market-linked, not guaranteed

- Historically higher long-term growth potential

- Better inflation-beating potential over 5+ years

- More liquidity in most categories (no lock-in beyond short exit-load windows)

👉 A practical, low-risk approach many beginners follow: use FDs or liquid funds for your emergency fund, and mutual funds for medium-to-long-term wealth creation. (Read our full mutual fund vs FD comparison if you’re still deciding between the two.)

Fixed Deposits typically offer 5%–7% depending on current FD rate trends set against the broader interest rate environment.

Neither fully replaces the other — they serve different jobs in your financial plan.

Advanced Tips for Beginners

1. Start Early

Time in the market is the single biggest lever in compounding. Even a smaller amount invested five years earlier can outperform a larger amount invested later.

2. Stay Invested Through Volatility

Market corrections are normal, not emergencies. Selling in a panic locks in a loss that a patient investor never actually experiences.

3. Increase Your SIP Gradually

A 10% annual step-up on your SIP, aligned with salary increments, can dramatically increase your final corpus without feeling like a bigger monthly burden.

4. Review Annually, Not Daily

Checking NAVs daily amplifies anxiety without adding any useful information. An annual review — checking if the fund still matches your goal and risk profile — is enough.

5. Rebalance Periodically

As your low-risk portfolio grows, periodically check whether your original debt-to-equity split still matches your goals, and rebalance if it has drifted significantly.

Final Thoughts on Best Mutual Fund for Beginners with Low Risk

The best mutual fund for beginners with low risk isn’t a single “magic scheme” — it’s a category and a discipline. Start with debt or balanced advantage funds, understand the Riskometer, use SIP to remove emotion from the equation, and add index funds only once you’re comfortable with the natural ups and downs of equity markets.

If you’re just starting out:

- ✔ Begin with an SIP, however small

- ✔ Choose debt or balanced advantage funds as your foundation

- ✔ Add index funds gradually as your risk comfort grows

- ✔ Keep your emergency fund completely separate, in a liquid fund or savings account

- ✔ Stay invested through market noise, and review only once or twice a year

👉 Wealth creation through mutual funds is a slow, steady process — and for beginners, “boring but consistent” almost always beats “exciting but erratic.”

Related Reads:

- Ready for more equity exposure? Compare index funds vs large-cap funds once you’re comfortable with market ups and downs.

- Not sure how much you can invest? Figure out your investable surplus first with a real salary budgeting example.

FAQs — Frequently Asked Questions

1.Which is the best mutual fund for beginners with low risk in India?

Debt funds and Balanced Advantage Funds are generally considered the safest starting categories, offering more stability than pure equity funds while still outperforming a savings account over time.

2. Can I lose money in low-risk mutual funds?

Yes. “Low risk” reduces the probability and magnitude of loss compared to equity funds, but it doesn’t eliminate risk entirely, since these are still market-linked investments, not guaranteed products.

3. What is the minimum amount needed to invest?

Most AMCs allow you to start an SIP with as little as ₹500–₹1,000 per month, and some even permit ₹100 for select schemes.

4. Are mutual funds better than FDs?

For long-term wealth creation, mutual funds generally offer higher growth potential than FDs, though FDs offer guaranteed returns and are better suited to short-term, zero-risk needs like an emergency fund.

5. Is SIP better than a lump sum investment for beginners?

For most beginners, yes — SIP reduces market-timing risk and builds a consistent investing habit, which matters more for long-term success than trying to pick the “perfect” entry point.

6. What does the SEBI Riskometer tell me?

It’s a mandatory, standardized six-level gauge (from “Low” to “Very High”) on every fund’s factsheet, showing at a glance how risky that specific scheme is considered by its own risk-value methodology.

7. How long should I stay invested in a low-risk mutual fund?

It depends on the category: liquid/debt funds suit goals within 1–3 years, while balanced advantage and index funds are better suited to 5+ year horizons to smooth out short-term volatility.

8. Do low-risk mutual funds have a lock-in period?

Most don’t have a formal lock-in (unlike ELSS tax-saving funds, which lock in for 3 years), but many charge a small exit load if you redeem within a specified short window — always check the scheme document.

9. Can I switch between fund categories later?

Yes. As your risk comfort and goals evolve, you can redeem from one category and reinvest in another, though be mindful of exit loads and the tax implications of redemption.

Disclaimer – Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Tax rules referenced here are subject to change; verify current rates with the Income Tax Department or a qualified tax advisor. This article is for educational purposes only and does not constitute financial, investment, or tax advice.

Shilpesh Rathod is the founder of All Finance Knowledge. He holds a B.Com degree along with JAIIB and CAIIB banking certifications, and brings 19+ years of experience in the banking sector across savings, investments, and financial planning.https://allfinanceknowledge.com/about-us/

1 thought on “Best Mutual Fund for Beginners with Low Risk in India (2026 Guide)”