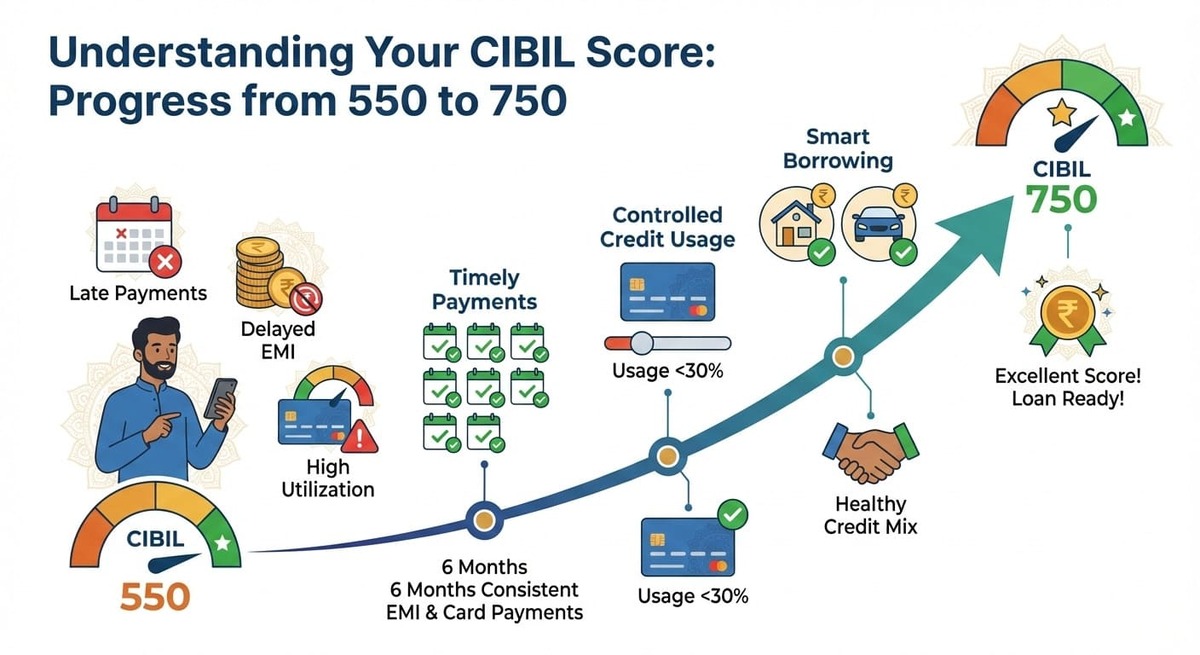

Improving your CIBIL score from 550 to 750 may seem difficult, but it is absolutely achievable with the right strategy and discipline. A low credit score can restrict your financial growth by limiting access to loans, increasing interest rates, or even leading to outright rejections.

The good news? Your credit score is not permanent. With consistent effort and smart financial habits, you can rebuild your credit profile and reach a strong score of 750 or above.

This detailed guide explains everything you need to know in simple language—perfect for beginners and anyone struggling with a low credit score in India.

What Does a CIBIL Score of 550 Mean?

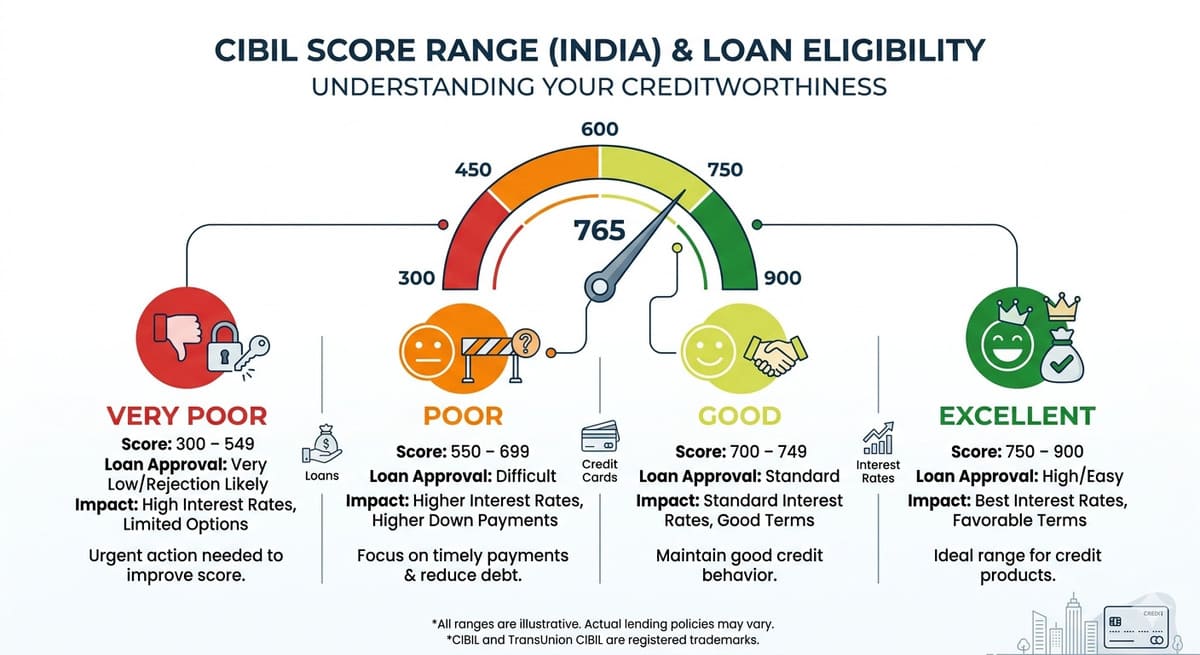

A CIBIL score ranges between 300 and 900 and represents your creditworthiness.

Credit Score Range in India

- 300–549: Very Poor

- 550–649: Poor to Fair

- 650–749: Good

- 750+: Excellent

A score of 550 typically indicates past credit issues such as:

- Missed EMIs or late payments

- Credit card defaults

- Loan settlements

- High credit utilization

- Multiple loan inquiries

Lenders consider this score risky, which is why improving it should be your top priority.

Is It Possible to Improve CIBIL Score from 550 to 750?

Yes, it is possible—but not instantly.

Realistic Expectations

- Improvement is gradual, not overnight

- It may take 6 to 18 months

- Requires consistent financial discipline

- No legal shortcut exists

Avoid agents or services promising “instant CIBIL score improvement”—these are often misleading.

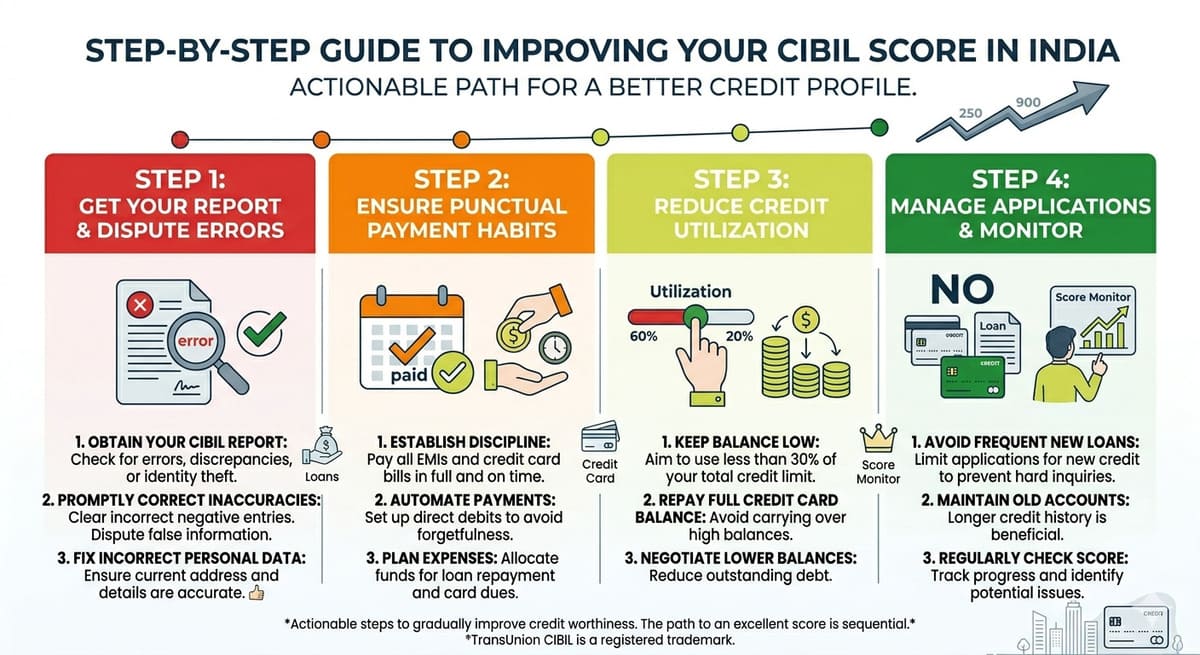

Step-by-Step Guide to Improve CIBIL Score from 550 to 750

Let’s break the process into clear and actionable steps.

Step 1: Check Your CIBIL Report Carefully

Start by downloading your latest credit report.

What to Check

- Incorrect personal details

- Wrong loan amounts

- Closed accounts marked as active

- Duplicate entries

- Unauthorized loans

Action Step

Raise a dispute immediately if you find errors. Even small corrections can boost your score.

Step 2: Clear All Pending Dues

Outstanding dues are the biggest reason for a low score.

What You Should Do

- Pay all overdue EMIs

- Clear credit card balances

- Avoid partial payments

- Close small pending amounts

Once your dues are cleared, your score starts improving within a few months.

Step 3: Always Pay EMIs and Bills on Time

Payment history contributes the highest weight in your credit score.

Best Practices

- Set up auto-debit

- Use payment reminders

- Pay 2–3 days before due date

Even one missed payment can reduce your score significantly, so consistency is key.

Step 4: Maintain Credit Utilization Below 30%

Credit utilization means how much of your credit limit you are using.

Example

- Credit Limit: ₹1,00,000

- Ideal Usage: Below ₹30,000

Pro Tip

Pay your credit card bill before the statement date, not just the due date. This keeps your utilization low in reports.

Step 5: Avoid Loan Settlements

Loan settlements may sound like relief but negatively impact your score.

Better Alternatives

- Request restructuring

- Negotiate repayment plans

- Convert dues into EMIs

If you have already settled a loan, don’t worry—its impact reduces over time with good behavior.

Step 6: Avoid Multiple Loan Applications

Every loan or credit card application creates a hard inquiry, which reduces your score slightly.

Smart Rule

- Maintain a gap of 3–6 months between applications

- Apply only when necessary

Too many inquiries signal financial stress to lenders.

Step 7: Keep Old Credit Accounts Active

Older accounts increase your credit age, which improves your score.

Tips

- Do not close old credit cards

- Use them occasionally

- Always pay in full

A long credit history builds trust with lenders.

Step 8: Use Secured Credit Options

If your score is very low and banks reject your applications, start small.

Options in India

- Secured credit card against FD

- Loan against fixed deposit

- Small gold loan

These are safe ways to rebuild your credit profile.

Step 9: Monitor Your Credit Score Regularly

Tracking your score helps you stay on the right path.

Benefits

- Detect errors early

- Track improvement

- Stay motivated

Checking your own credit score does not reduce it.

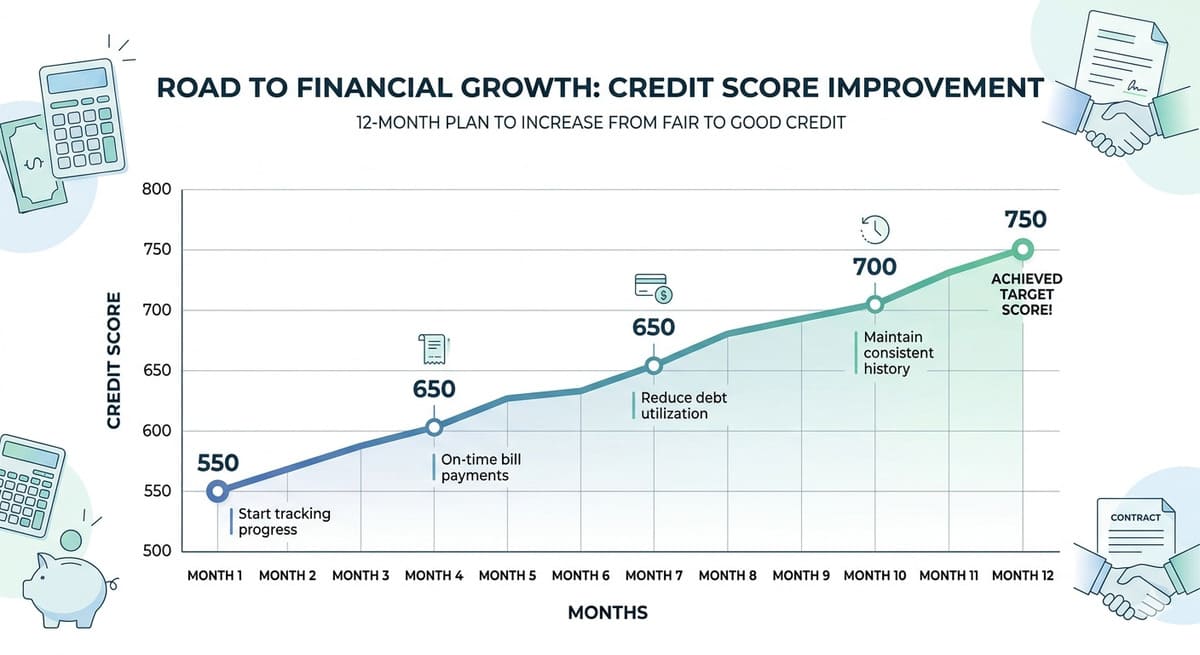

How Long Will It Take to Reach 750?

Here’s a realistic timeline:

| Action | Expected Impact Time |

|---|---|

| Clearing dues | 1–3 months |

| Regular payments | 3–6 months |

| Reducing utilization | 2–4 months |

| Major improvement | 6–18 months |

Patience and discipline are essential.

Advanced Tips to Boost Your CIBIL Score Faster

If you want quicker improvement, follow these expert strategies:

1. Increase Credit Limit

Request a higher limit from your bank to reduce utilization ratio.

2. Use Credit Mix

Maintain a balance of secured (home loan) and unsecured loans (credit card).

3. Pay More Than Minimum Due

Always pay full outstanding amount—not just minimum due.

4. Avoid Closing Multiple Accounts

Closing accounts reduces your credit history length.

Common Mistakes to Avoid

Avoid these errors while improving your score:

- Paying only minimum due

- Ignoring small overdue amounts

- Closing all credit accounts

- Applying for too many loans

- Using illegal credit repair services

FAQs: Improve CIBIL Score from 550 to 750

1. Can I improve my CIBIL score quickly?

There is no instant method, but disciplined behavior shows results within months.

2. Does checking CIBIL score reduce it?

No, self-checks do not affect your score.

3. Will paying one EMI boost my score?

Yes, but consistent payments matter more.

4. Can loan settlement be removed?

No, but its impact reduces over time.

5. Is 750 a good CIBIL score?

Yes, it is considered very good by most lenders.

6-Can I Improve CIBIL Score from 550 to 750?

Yes one can improve CIBIL score from 550 to 750 but it takes time.

Final Thoughts

Improving your CIBIL score from 550 to 750 is a journey that requires patience, discipline, and the right strategy. Focus on paying dues on time, reducing credit utilization, avoiding unnecessary loans, and maintaining a healthy credit profile.

Remember, financial improvement is not about quick fixes—it’s about building long-term habits. Stay consistent, and your score will gradually rise, opening doors to better financial opportunities.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Credit score improvement timelines and results may vary based on individual credit profiles.

Shilpesh Rathod is the founder of All Finance Knowledge. He holds a B.Com degree along with JAIIB and CAIIB banking certifications, and brings 19+ years of experience in the banking sector across savings, investments, and financial planning. Read more: https://allfinanceknowledge.com/about-us/