February 4, 2026 by Shilpesh Rathod

Does checking CIBIL score reduce credit score in India?

This is one of the most common doubts among Indian borrowers. Many people avoid checking their CIBIL score because they believe it might reduce their credit score and affect loan eligibility.

But is this really true?

The short answer is NO—checking your own CIBIL score does not reduce your credit score.

However, the confusion arises due to a lack of clarity between different types of credit enquiries. In this detailed and beginner-friendly guide, we will explain everything you need to know about how CIBIL score checks work, the difference between hard and soft enquiries, and how to monitor your credit score safely without harming it.If you are already tracking your score but not seeing changes, you should understand why CIBIL score is not updating and how to fix it.

What Is a CIBIL Score?

A CIBIL score is a three-digit number ranging from 300 to 900, calculated by TransUnion CIBIL. It represents your creditworthiness based on your past financial behaviour. You can check your CIBIL report directly from the official website.

Credit Score Ranges in India

- 750 and above – Excellent

- 700–749 – Good

- 650–699 – Average

- Below 650 – Poor

As per RBI guidelines on credit discipline, maintaining a good repayment history is essential.

Banks, NBFCs, and lenders use this score to decide:

- Whether to approve your loan

- What interest rate to offer

- Your credit card eligibility

- Your repayment capacity

A higher score increases your chances of approval and helps you get better financial deals.

Does Checking CIBIL Score Reduce Credit Score?

✅ Short Answer: NO

Checking your own CIBIL score does NOT reduce your credit score.

This is a common myth in India. In fact, regularly checking your score is considered a good financial habit because it helps you stay aware of your credit health.

The confusion usually happens when people mix up self-checks with loan applications.

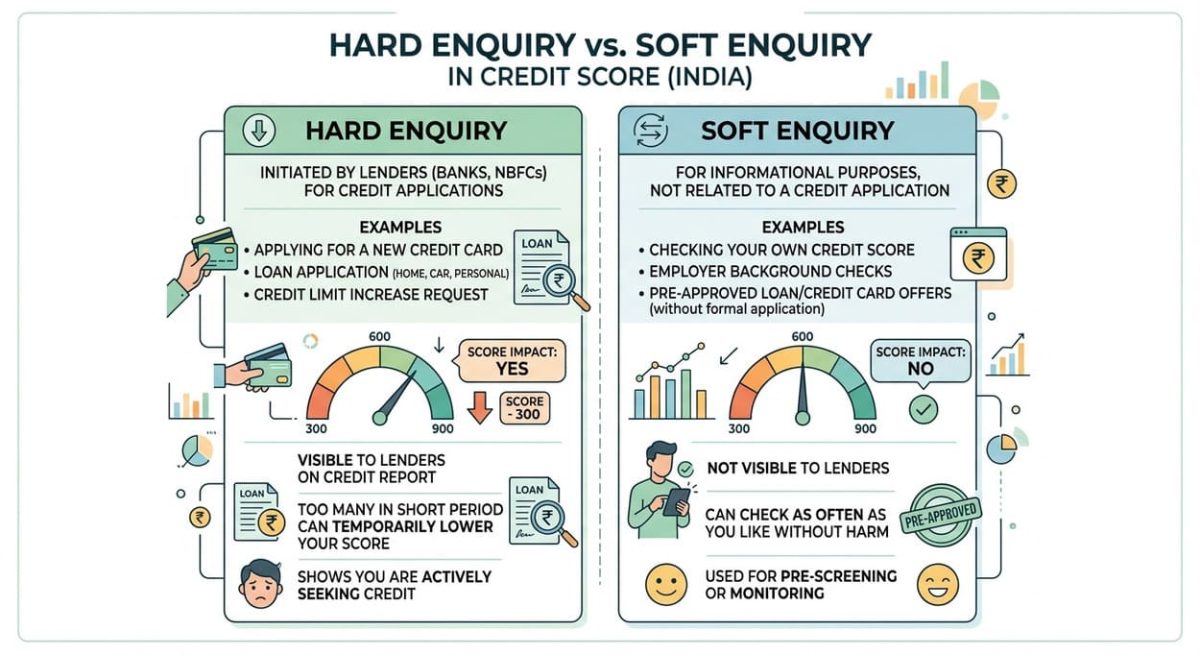

Understanding Credit Enquiries: Hard vs Soft

To fully understand this concept, you need to know the two types of credit enquiries.

1️⃣ Soft Enquiry (No Impact on Score)

A soft enquiry occurs when:

- You check your own credit score

- Banks check your profile for pre-approved offers

- Credit apps show your score

Key Features of Soft Enquiry:

- ✅ No impact on credit score

- ✅ Not visible to lenders

- ✅ Can be done unlimited times

- ✅ Safe and recommended

Examples:

- Checking score on official CIBIL website

- Viewing score in your banking app

- Using RBI-regulated financial apps

👉 So, you can check your score every month without any worry.

2️⃣ Hard Enquiry (May Reduce Score)

A hard enquiry happens when:

- You apply for a loan

- You apply for a credit card

- You request a credit limit increase

Key Features of Hard Enquiry:

- ⚠️ May reduce score by 5–10 points

- ⚠️ Visible to lenders

- ⚠️ Multiple enquiries indicate high credit dependency

Important Note:

One or two enquiries are normal. But applying to multiple loans in a short period can negatively impact your score.

Why Do People Think Checking CIBIL Score Reduces It?

This myth is very common, and here’s why it exists:

- People check their score before applying for a loan

- Then they apply for a loan (hard enquiry happens)

- Score drops slightly

- They assume the self-check caused the drop

👉 In reality, the loan application caused the drop—not the score check.

How Often Should You Check Your CIBIL Score?

Monitoring your credit score regularly is important for maintaining financial health.

Recommended Frequency:

- Once every 1–3 months

- Before applying for any loan

- After closing a loan or credit card

- When improving your score

There is no limit on soft enquiries, so you can check as often as needed.

Benefits of Checking Your CIBIL Score Regularly

Regular monitoring offers several advantages:

1. Avoid Loan Rejections

You can apply for loans only when your score is strong.

2. Get Better Interest Rates

Higher scores help you negotiate lower EMIs.

3. Detect Errors Early

Sometimes reports contain mistakes that can reduce your score.

4. Prevent Fraud

You can identify unauthorisedf loans or credit cards.

5. Track Improvement

If you’re working to improve your score (e.g., from 550 to 750), monitoring helps measure progress.

If your score is low, you can follow this complete guide to improve CIBIL score from 550 to 750 step-by-step.f

Does Checking CIBIL Score Through Apps Reduce It?

No, checking your score through apps does not reduce it, provided the app:

- Uses soft enquiry (soft pull)

- Is regulated or trustworthy

- Clearly mentions credit report source

Safe Platforms Include:

- Official CIBIL website

- Bank mobile apps

- Trusted financial apps

👉 Avoid apps that ask for unnecessary permissions or sensitive data.

Common Myths About CIBIL Score Checking

Let’s clear some common misconceptions:

❌ Checking your score multiple times reduces it

❌ Free credit score checks are unsafe

❌ Only banks can access credit scores

✅ Reality:

- Self-checks are always safe

- Free reports from trusted platforms are reliable

- You have full access to your own credit information

Best Practices for Safe CIBIL Score Monitoring

Follow these simple tips to maintain a healthy credit profile:

- Use only trusted platforms

- Check your full report—not just the score

- Avoid frequent loan applications

- Keep track of credit enquiries

- Maintain timely repayments

Advanced Tips to Protect and Improve Your Credit Score

If you want to go beyond basics, follow these expert tips:

1. Keep Credit Utilization Below 30%

Using too much of your credit limit can lower your score.

2. Maintain a Good Credit Mix

Balance between secured and unsecured loans.

3. Avoid Closing Old Accounts

Older accounts improve your credit history length.

4. Pay More Than Minimum Due

Always try to pay full outstanding balance.

When Does a Credit Score Actually Drop?

Your score may reduce due to:

- Missed EMIs or late payments

- High credit card usage

- Loan settlements

- Multiple hard enquiries

- Defaulted loans

👉 Checking your score is NOT one of the reasons.

FAQs: Does Checking CIBIL Score Reduce Credit Score?

Q1. Does checking CIBIL score online reduce points?

No, self-checks are soft enquiries and do not affect your score.

Q2. How much score drops due to hard enquiry?

Usually 5–10 points, and it recovers with timely repayments.

Q3. Is checking score every month safe?

Yes, it is completely safe.

Q4. Can banks see my self‑checks?

No. Soft enquiries are not visible to lenders.

Q5. Is it good to check the CIBIL score before a loan application?

Yes. It helps avoid rejection.

Final Thoughts

Understanding whether checking your CIBIL score reduces it is important for making confident financial decisions. The truth is simple: checking your own credit score is completely safe and does not harm your credit profile.

In fact, regular monitoring helps you stay informed, detect errors early, and improve your financial discipline. Instead of avoiding your credit report, make it a habit to check it regularly and take corrective actions when needed.

By maintaining timely repayments, controlling credit usage, and avoiding unnecessary loan applications, you can build a strong credit profile and achieve a score above 750 over time.

To build long-term financial stability, follow a structured personal finance planning guide.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Credit score rules may vary by lender, so always verify details with official sources before making financial decisions.

Shilpesh Rathod is the founder of All Finance Knowledge. He holds a B.Com degree along with JAIIB and CAIIB banking certifications, and brings 19+ years of experience in the banking sector across savings, investments, and financial planning. Read more: https://allfinanceknowledge.com/about-us/