Lets understand the Home Loan EMI Calculation with Real Example: A Complete Guide for 2026

Buying a house is one of the biggest financial decisions in life. For most people in India, taking a home loan is not just an option—it is a necessity. But before you sign any loan agreement, you must clearly understand home loan EMI calculation with a real example.

Many borrowers make the mistake of focusing only on the interest rate. However, your EMI depends on three major factors: loan amount, interest rate, and tenure. A small change in any of these can add or save lakhs of rupees.

In this guide, we will break down everything in simple, everyday language. You will learn how EMI works, see a real-life calculation, and understand smart strategies to reduce your loan burden.

What Is Home Loan EMI?

EMI stands for Equated Monthly Installment.

It is the fixed amount you pay every month to repay your home loan. Your EMI automatically includes two components:

- Principal amount – the actual loan you borrowed.

- Interest amount – the cost charged by the bank for lending you money.

Important pattern to remember:

- In the first few years, the interest portion of your EMI is very high, and the principal repayment is low.

- In the later years, the principal portion becomes higher, and interest reduces.

This structure is called amortization. Banks design it this way to recover their interest early in the loan tenure.

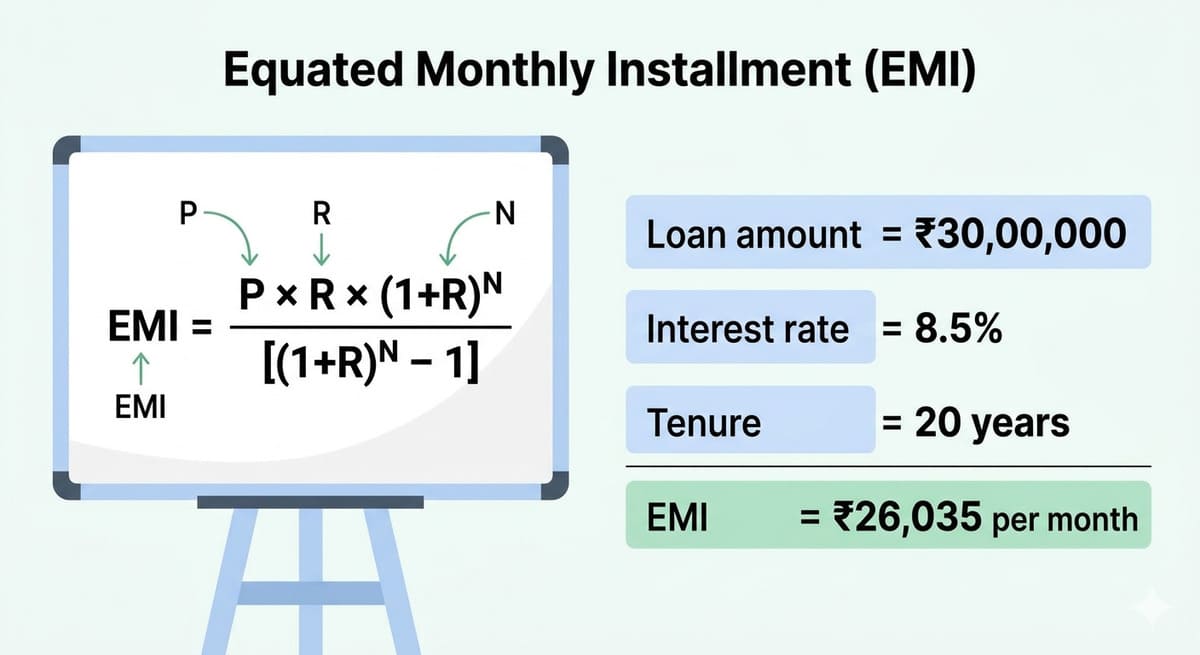

Home Loan EMI Calculation Formula (Standard)

Banks and housing finance companies use a standard mathematical formula to calculate EMI:

EMI = P × R × (1 + R)^N / [(1 + R)^N – 1]

Where:

- P = Principal loan amount (in rupees)

- R = Monthly interest rate (annual rate ÷ 12 ÷ 100)

- N = Loan tenure in months

Do not worry if the formula looks complicated. Let us now understand it with a real example that you can relate to.

Home Loan EMI Calculation with Real Example

Let us take a typical scenario for a middle-class family in India.

Loan details:

- Loan Amount (P) = ₹30,00,000 (30 lakhs)

- Annual Interest Rate = 8.5% per year

- Loan Tenure = 20 years

Step 1 – Convert annual interest to monthly rate

8.5% ÷ 12 ÷ 100 = 0.007083

Step 2 – Convert tenure into months

20 years × 12 = 240 months

Step 3 – Apply the EMI formula

EMI = 30,00,000 × 0.007083 × (1 + 0.007083)^240 / [(1 + 0.007083)^240 – 1]

After calculation, the EMI comes to approximately:

₹26,035 per month

So, if you take a ₹30 lakh home loan for 20 years at 8.5% interest, you will pay around ₹26,000 every month for the next 20 years.

Total Interest You Will Pay – The Reality Check

Many borrowers forget to calculate total interest. Let us do that now.

- Monthly EMI = ₹26,035

- Total months = 240

Total repayment = ₹26,035 × 240 = ₹62,48,400

- Loan amount (principal) = ₹30,00,000

- Total interest paid = ₹32,48,400

Yes, you read that correctly.

You are paying more than the principal amount in interest alone.

This is exactly why understanding home loan EMI calculation with a real example is so important before signing any loan agreement.

EMI Breakdown: First Year vs Last Year

Let us see how your EMI is divided over time.

In the first year:

- Interest portion: very high (~80% of EMI)

- Principal portion: very low (~20% of EMI)

After 10 years:

- Interest and principal become roughly equal

In the last year:

- Principal portion: very high (~95% of EMI)

- Interest portion: very low (~5% of EMI)

This means if you try to close your loan early, you save a lot of interest. But if you close it very late, most of the interest has already been paid.

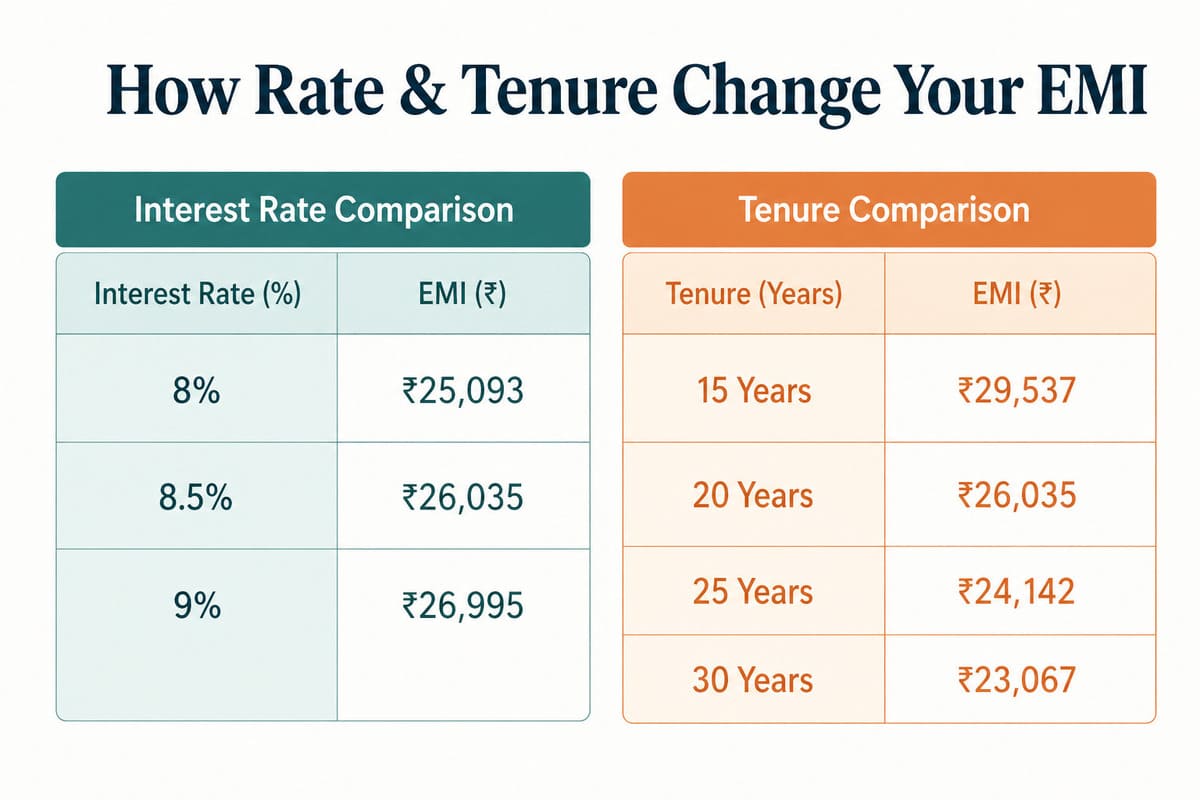

How Interest Rate Affects Your EMI

A small difference in interest rate has a big impact. Let us compare the same ₹30 lakh loan for 20 years at different rates.

| Interest Rate | Monthly EMI | Total Interest |

|---|---|---|

| 8.0% | ₹25,093 | ₹30,22,320 |

| 8.5% | ₹26,035 | ₹32,48,400 |

| 9.0% | ₹26,995 | ₹34,78,800 |

Key takeaway: Even a 0.5% increase adds over ₹2 lakh to your total interest.

How Loan Tenure Affects Your EMI

You can choose a shorter or longer tenure. Each has trade-offs.

Example: ₹30 lakh loan at 8.5% interest

| Tenure | Monthly EMI | Total Interest |

|---|---|---|

| 15 years | ₹29,537 | ₹23,16,660 |

| 20 years | ₹26,035 | ₹32,48,400 |

| 25 years | ₹24,142 | ₹42,42,600 |

| 30 years | ₹23,067 | ₹53,04,120 |

- Shorter tenure = higher EMI but much lower total interest.

- Longer tenure = lower EMI but much higher total interest.

Smart rule: Choose the shortest tenure you can comfortably afford.

Before applying, always check your CIBIL score as it directly impacts your interest rate.”

Should You Use an EMI Calculator?

Instead of manual math, always use an online EMI calculator. It is fast, free, and accurate.

You can find reliable calculators on:

- RBI website – for official awareness

- SEBI investor portal – for unbiased calculations

✅ Always check at least two different EMI calculators before finalizing your loan.

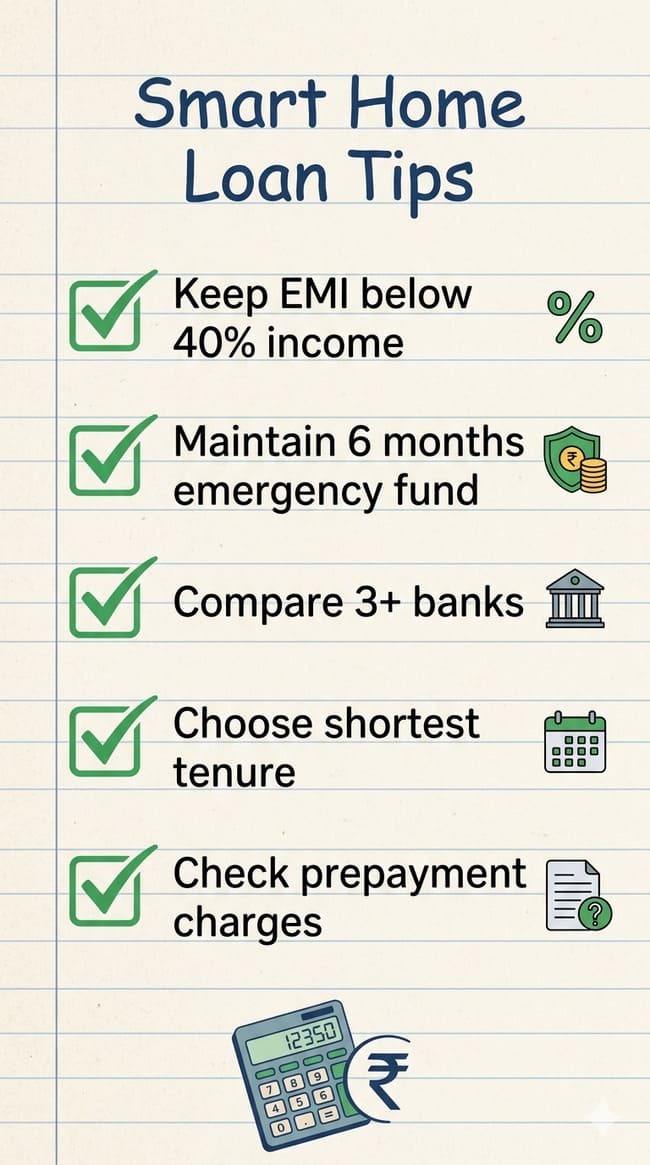

Smart Tips Before Taking a Home Loan

Follow these practical rules to stay financially safe.

1. Keep EMI below 40% of your monthly income

If your monthly income is ₹70,000, your home loan EMI should not exceed ₹28,000.

2. Maintain an emergency fund

Keep at least 6 months of EMI in a separate savings account.

3. Compare at least 3 banks

Do not accept the first offer. Public banks, private banks, and NBFCs all have different rates.

4. Check prepayment and foreclosure charges

Many banks do not charge for floating-rate loans. Avoid loans with high prepayment penalties.

5. Read the loan amortisation schedule

This is a table showing exactly how much principal and interest you pay each month. Ask your bank for it.

Can You Reduce Your Home Loan EMI After Taking It?

Yes, you can reduce your EMI in several ways:

- Make a partial prepayment – pay extra whenever you have surplus money.

- Increase your down payment at the time of purchase.

- Negotiate a lower interest rate with your existing bank.

- Transfer your loan to another bank offering a lower rate (balance transfer).

- Reduce tenure instead of EMI – this saves more interest.

Even one extra EMI payment every year can reduce your loan tenure by several years.

Fixed vs Floating Interest Rate – Which Is Better?

Fixed Interest Rate:

- EMI remains constant throughout the tenure.

- Safe during rising interest rate markets.

- Usually 1–2% higher than floating rates.

Floating Interest Rate:

- EMI changes when RBI changes repo rate.

- Can go up or down.

- Historically cheaper over long periods.

Recommendation: Most salaried borrowers should choose floating rate for a 15–20 year loan because it offers flexibility and lower initial cost.

Interest rates change based on the repo rate set by Reserve Bank of India

Common Mistakes to Avoid

- ❌ Taking a longer tenure just to get a lower EMI.

- ❌ Ignoring total interest payable.

- ❌ Not checking processing fees and hidden charges.

- ❌ Applying for a loan without checking your CIBIL score first.

- ❌ Believing that a lower EMI means a better loan.

Final Thought

Understanding home loan EMI calculation with a real example is not just a mathematical exercise—it is a financial survival skill. A home loan is a 15-to-30-year commitment. A small mistake in tenure or rate can cost you lakhs of rupees.

Before applying for any housing loan, always calculate:

- Monthly EMI

- Total interest payable

- Impact on your monthly budget

Then ask yourself honestly: Can I pay this EMI for 20 years without stress?

If yes, you are ready. If not, wait, save more, or choose a smaller loan.

Borrow wisely. Plan carefully. And always keep learning.

Frequently Asked Questions (FAQ)

1. What is EMI in a home loan?

Ans- EMI is the fixed monthly amount you pay to repay both principal and interest.

2. How is home loan EMI calculated?

Ans- It is calculated using principal, interest rate, and tenure with the formula:

EMI = P × R × (1 + R)^N / [(1 + R)^N – 1]

3. Does a longer tenure reduce EMI?

Ans- Yes, but it increases total interest paid significantly.

4. Can I reduce my home loan EMI after taking the loan?

Ans – Yes, by prepaying, negotiating a lower rate, or transferring the loan.

5. Is EMI affected by floating interest rates?

Ans – Yes, RBI policy changes can increase or decrease your EMI.

6. What is a good EMI-to-income ratio?

Ans – Ideally, home loan EMI should not exceed 40% of your monthly take-home salary.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial advice. Interest rates, tax laws, and bank policies change over time. Please consult your bank or a SEBI-registered financial advisor before making any home loan decision.

1 thought on “Home Loan EMI Calculation with Real Example: A Complete Guide for 2026”