The 50-30-20 rule in India is a simple budgeting method that helps salaried individuals manage expenses, savings, and investments effectively. Managing money can feel overwhelming, especially when income is limited and expenses keep rising. Many Indians earn a fixed monthly salary but still struggle with savings, investments, and unexpected expenses. This is where the 50-30-20 rule in india becomes extremely useful. It is a simple budgeting formula that helps you divide your income smartly without complicated calculations.

In this detailed guide, we will explain the 50-30-20 rule in india using Indian salary examples, making it easy for beginners, working professionals, and families. The article is written in simple language

What Is the 50-30-20 Rule in India?

The 50-30-20 rule is a popular budgeting method that divides your monthly income into three parts:

- 50% for Needs – Essential expenses you cannot avoid

- 30% for Wants – Lifestyle and discretionary spending

- 20% for Savings & Investments – Your financial future

This rule was popularized to make budgeting simple and flexible. Instead of tracking every rupee, you focus on percentages, which makes it easier to stick to a budget.

Why the 50-30-20 Rule Works Well in India

Indian households have unique financial challenges:

- Rising cost of living

- EMIs and loans

- Family responsibilities

- Irregular bonuses and incentives

The 50-30-20 rule works well because:

- It is easy to understand

- It encourages habitual saving

- It balances present enjoyment and future security

- It can be adjusted for different income levels

Whether you earn ₹20,000 or ₹2,00,000 per month, the concept remains the same.

50-30-20 Rule Explained with Indian Salary Example

Let us understand this with a practical Indian salary example.

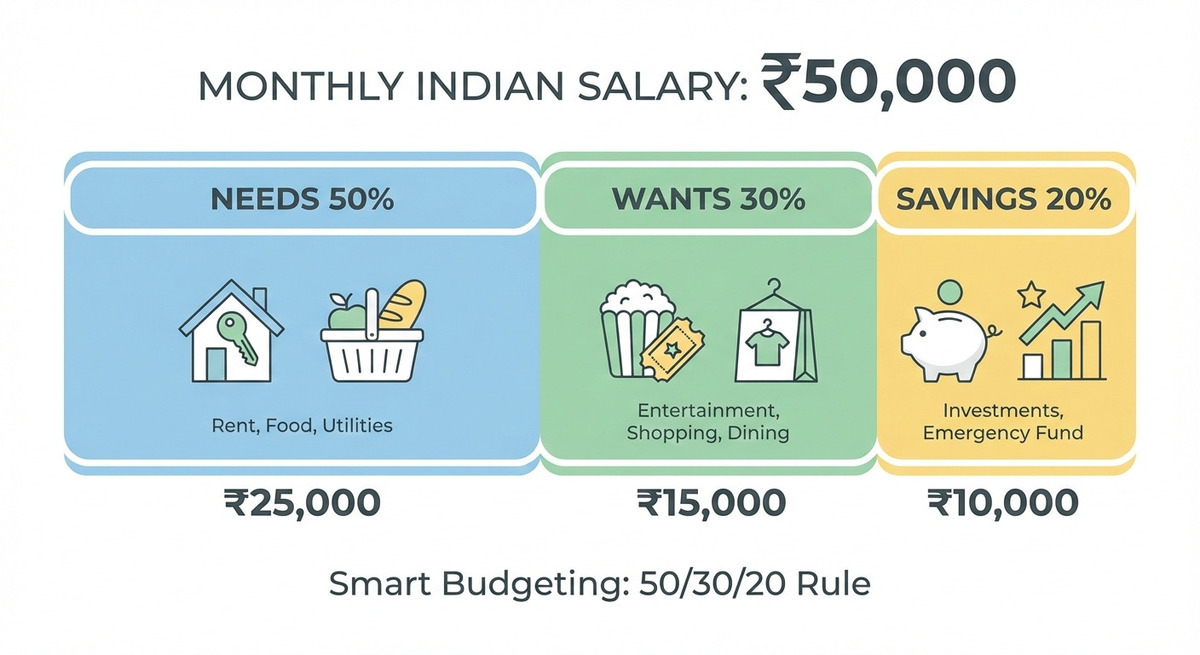

Example: Monthly Salary ₹50,000

If your monthly take-home salary is ₹50,000, the rule suggests:

- 50% Needs = ₹25,000

- 30% Wants = ₹15,000

- 20% Savings = ₹10,000

Now let’s break this down further.

50-30-20 Rule vs Traditional Budgeting in India

Many Indian households follow traditional budgeting, where expenses are tracked without a fixed structure. While this works for some, it often leads to confusion and inconsistent savings.

Traditional Budgeting Problems:

- No fixed savings target

- Overspending on lifestyle

- Savings happen only if money is left

- Difficult to track every expense

50-30-20 Rule Advantage:

👉 This rule simplifies everything:

- Clear allocation of income

- Fixed savings habit

- Better financial discipline

- Less stress about money management

📌 Instead of tracking every rupee, you focus on smart distribution of income.

🔹 Monthly Budget Planning Using 50-30-20 Rule

To apply this rule effectively, you need a simple monthly plan.

Step-by-Step Budget Plan:

Step 1: Calculate Take-Home Salary

Always use your in-hand salary, not CTC.

Step 2: Divide into 3 Categories

- Needs (50%)

- Wants (30%)

- Savings (20%)

Step 3: Track Your Expenses

Use apps or a simple notebook.

Step 4: Adjust Where Needed

If needs exceed 50%, reduce wants.

Step 5: Automate Savings

Transfer savings amount immediately after salary credit.

📌 This method ensures you stay consistent every month.

🔹 Real-Life Example: Metro City vs Small Town

The 50-30-20 rule works differently depending on where you live.

Metro City (e.g., Mumbai, Bangalore)

Salary: ₹60,000

- Needs: ₹35,000–₹40,000 (higher rent)

- Wants: ₹10,000–₹15,000

- Savings: ₹5,000–₹10,000

Small Town

Salary: ₹40,000

- Needs: ₹18,000–₹22,000

- Wants: ₹8,000–₹10,000

- Savings: ₹8,000–₹12,000

📌 Cost of living plays a big role. Adjust percentages based on reality.

🔹 How to Increase Savings Beyond 20%

Saving 20% is a great start—but increasing it can accelerate wealth creation.

Practical Tips:

✔ Increase income (side hustle, freelancing)

✔ Avoid lifestyle inflation

✔ Cut unnecessary subscriptions

✔ Use bonuses for investing

✔ Reduce high-interest loans

📌 Even increasing savings from 20% to 30% can significantly improve your future wealth.

🔹 Role of Emergency Fund in 50-30-20 Rule

Before investing aggressively, building an emergency fund is essential.

What Is an Emergency Fund?

Money set aside for:

- Medical emergencies

- Job loss

- Unexpected expenses

Ideal Amount:

👉 3–6 months of expenses

Where to Keep It?

- Savings account

- Fixed deposit

- Liquid mutual fund

📌 This protects you from financial stress and prevents debt.

🔹 How 50-30-20 Rule Helps in Financial Goals

This rule is not just about budgeting—it helps you achieve life goals.

Short-Term Goals:

- Buying a phone

- Travel

- Emergency fund

Medium-Term Goals:

- Car purchase

- Higher education

Long-Term Goals:

- House

- Retirement

- Children’s education

👉 Your 20% savings portion fuels all these goals.

🔹 Mistakes Indians Make While Budgeting

Even with a good rule, mistakes can happen.

❌ Not separating needs and wants clearly

❌ Ignoring inflation

❌ Not reviewing budget monthly

❌ Overspending during festivals or sales

❌ Not increasing savings with income

📌 Awareness of these mistakes improves financial discipline.

🔹 Digital Tools to Track Budget in India

Tracking expenses becomes easier with apps.

Popular Options:

- Walnut

- Money Manager

- ET Money

- Bank apps

You can also use:

- Excel sheets

- Simple notebook

📌 Tracking helps you stick to the 50-30-20 rule consistently.

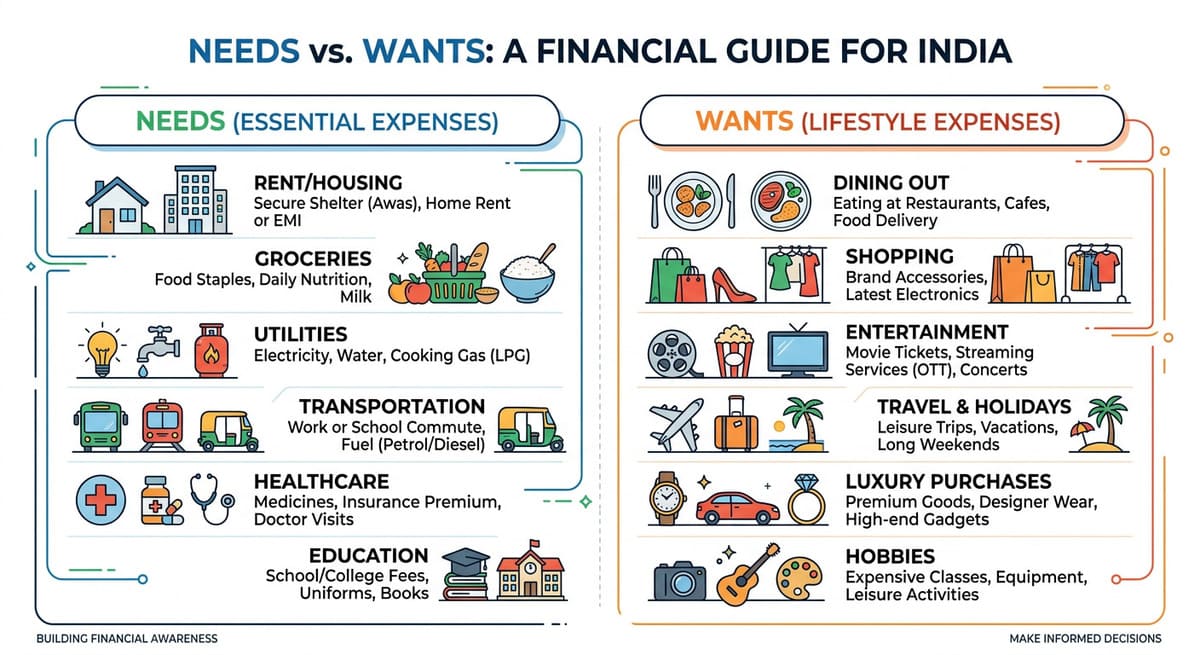

50% – Needs (Essential Expenses)

Needs are expenses that are necessary for survival and basic living. These are non-negotiable expenses.

Common Needs in an Indian Household

- House rent or home loan EMI

- Groceries and daily food expenses

- Electricity, water, gas bills

- Mobile and internet bills

- School or college fees

- Basic transportation (bus, train, fuel)

- Insurance premiums (health, term)

Example Allocation (₹25,000)

- Rent: ₹12,000

- Groceries: ₹6,000

- Utilities & mobile: ₹2,500

- Transport: ₹2,000

- Insurance: ₹2,500

Tip: If your needs exceed 50%, you should try reducing EMIs, shifting to a cheaper house, or cutting unnecessary subscriptions.

Understanding needs vs wants helps you control spending effectively.

30% – Wants (Lifestyle Expenses)

Wants are expenses that improve your lifestyle but are not essential.

Common Wants in India

- Eating out and food delivery

- OTT subscriptions (Netflix, Prime, Hotstar)

- Shopping for clothes and gadgets

- Vacations and weekend trips

- Gym memberships

- Entertainment and hobbies

Example Allocation (₹15,000)

- Dining out: ₹4,000

- OTT & apps: ₹1,000

- Shopping: ₹5,000

- Movies & outings: ₹3,000

- Miscellaneous fun: ₹2,000

This category allows you to enjoy life without guilt, as long as it stays within limits

20% – Savings & Investments (Your Future)

This is the most important part of the 50-30-20 rule. It ensures long-term financial stability.

Where Should Indians Invest the 20%?

- Emergency fund (6 months expenses)

- SIP in mutual funds

- Public Provident Fund (PPF)

- Employee Provident Fund (EPF)

- National Pension System (NPS)

- Fixed Deposits (FDs)

- Recurring Deposits (RDs)

Example Allocation (₹10,000)

- SIP in equity mutual fund: ₹5,000

- PPF / EPF: ₹3,000

- Emergency fund: ₹2,000

Golden rule: Pay yourself first. Automate savings as soon as salary is credited.

How to Apply the 50-30-20 Rule on a Low Salary

If you earn ₹20,000–₹30,000 per month, strict 50-30-20 may feel difficult. In such cases, you can modify it:

- 60% Needs

- 20% Wants

- 20% Savings

Even saving ₹1,000–₹2,000 per month consistently can make a big difference over time.

50-30-20 Rule for Families vs Singles

For Singles

- Higher spending on wants

- Lower family responsibilities

- Easier to save 20% or more

For Families

- Higher needs due to children and EMIs

- Savings may start lower but should grow with income

The rule is flexible, not rigid.

Benefits of the 50-30-20 Rule

- Simple and beginner-friendly

- Reduces financial stress

- Encourages disciplined saving

- Improves money awareness

- Works with Indian salaries

50-30-20 Rule vs Other Budgeting Methods

There are other budgeting methods, but this one is the simplest.

Zero-Based Budget

- Every rupee is assigned a job

- More detailed but time-consuming

Envelope Method

- Cash-based system

- Useful but less practical today

50-30-20 Rule

- Simple

- Flexible

- Beginner-friendly

👉 That’s why it is ideal for most Indian earners.

Common Mistakes to Avoid

- Ignoring savings completely

- Treating wants as needs

- Not tracking expenses at all

- Depending only on salary hikes

FAQs on the 50-30-20 Rule

1. Is the 50-30-20 rule suitable for Indians?

Yes, it works very well when adapted to Indian income and expenses

2. Can I change the percentages?

Yes, the rule is flexible based on your income and responsibilities.

3. Does the rule include tax?

It is calculated on take-home salary, not gross income.

4. Is saving 20% mandatory?

It is recommended, but even 10–15% is a good start.

5. Can business owners use this rule?

Yes, by applying it to average monthly income

Q6. Can I follow 50-30-20 rule with irregular income?

Yes, use average monthly income as a base.

Q7. Should I include EMIs in needs?

Yes, EMIs are part of essential expenses.

Q8. Can I save more than 20%?

Yes, higher savings lead to faster wealth creation.

Final Thoughts

The 50-30-20 rule is one of the simplest and most effective ways to manage money, especially for Indian salaried individuals. You do not need high income or financial expertise—just discipline and consistency. Start small, stay consistent, and let time and compounding work in your favor.

Disclaimer : This article is for educational and informational purposes only. Please consult a certified financial advisor before making any investment or financial decisions.

2 thoughts on “50-30-20 Rule in India Explained with Indian Salary Example”