CIBIL score explained clearly helps you understand how your credit score works and how it affects loans, credit cards, and interest rates in India.. Many people hear the term “CIBIL score” but do not fully understand how it works or how to improve it quickly.

In this guide, we will explain what a CIBIL score is, why it matters, how it is calculated, and practical steps to improve it fast—especially for beginners.

🔹CIBIL Score Explained in Simple Language?

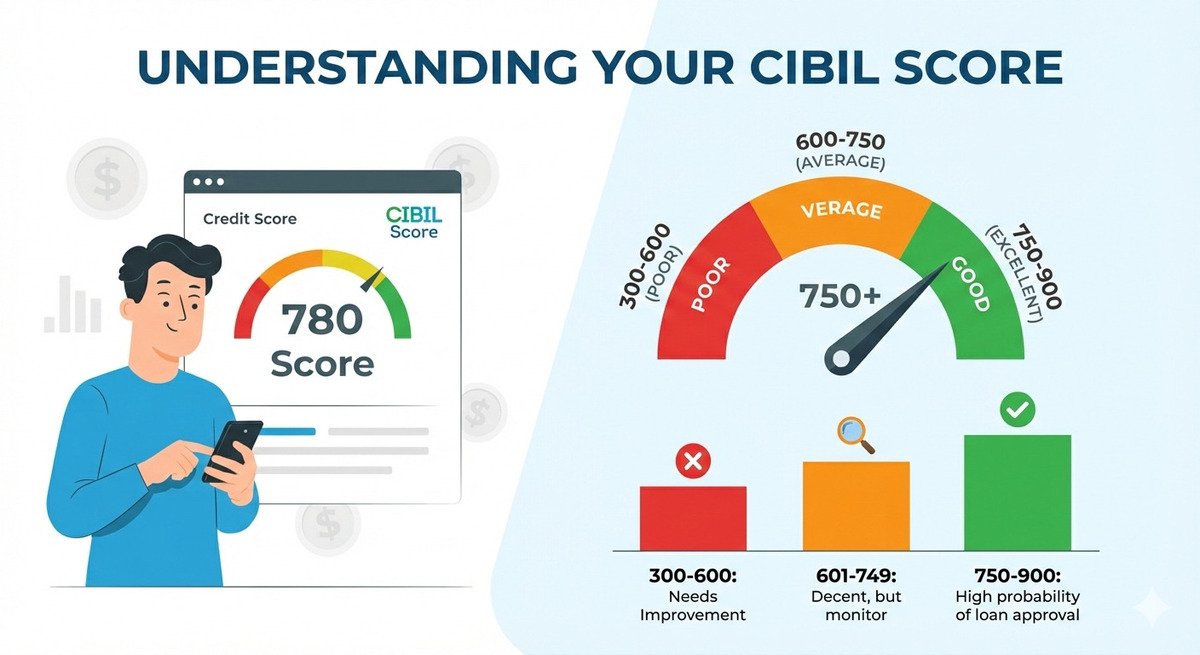

A CIBIL score is a three-digit number that represents your creditworthiness. It is issued by TransUnion CIBIL, one of India’s leading credit bureaus.

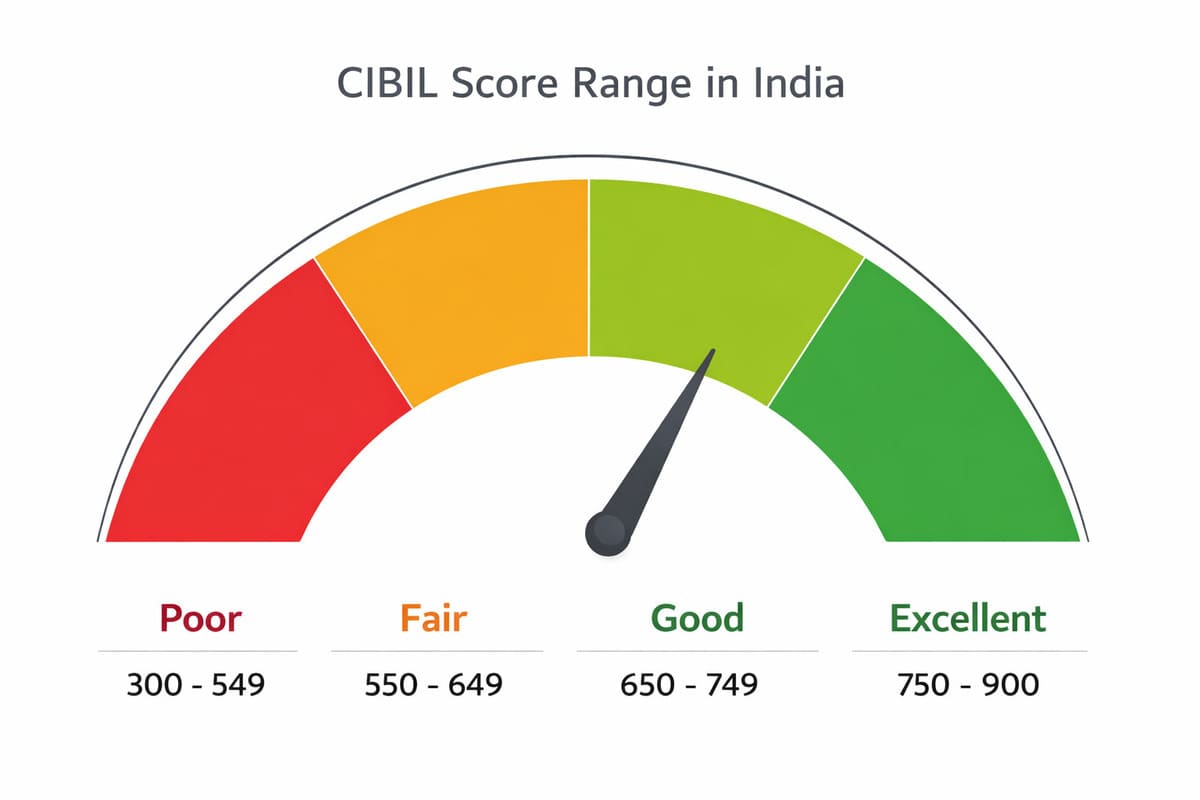

📊 CIBIL Score Range:

- 300 – 549: Poor

- 550 – 649: Fair

- 650 – 749: Good

- 750 – 900: Excellent

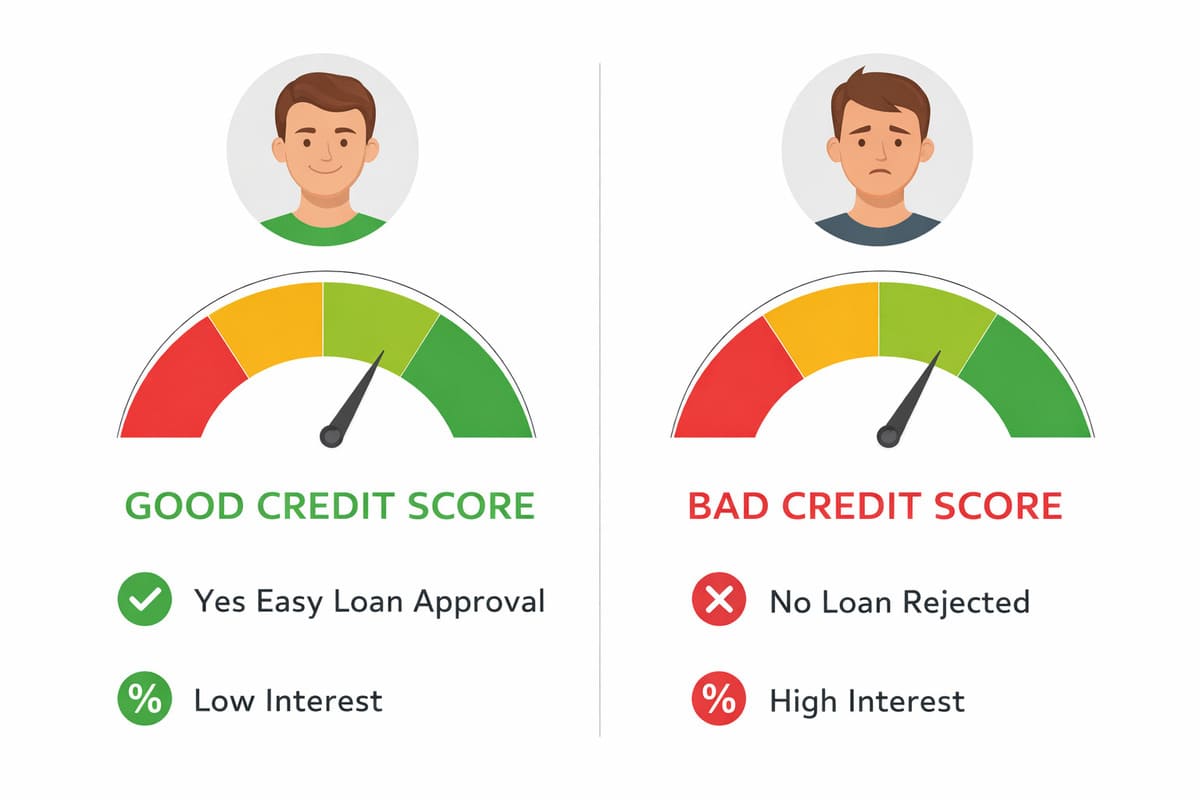

Banks and NBFCs use this score to evaluate how responsibly you handle credit. A higher score increases your chances of loan approval at lower interest rates.

CIBIL score categories range from poor to excellent in India.

🔹 Why Is CIBIL Score Important?

Your CIBIL score impacts multiple financial decisions:

- ✔ Faster loan approvals

- ✔ Lower interest rates

- ✔ Higher credit card limits

- ✔ Better negotiation power with banks

- ✔ Approval for premium financial products

A low CIBIL score, on the other hand, may lead to loan rejection or high interest rates.

A higher CIBIL score improves the chances of loan approval and lowers interest rates.

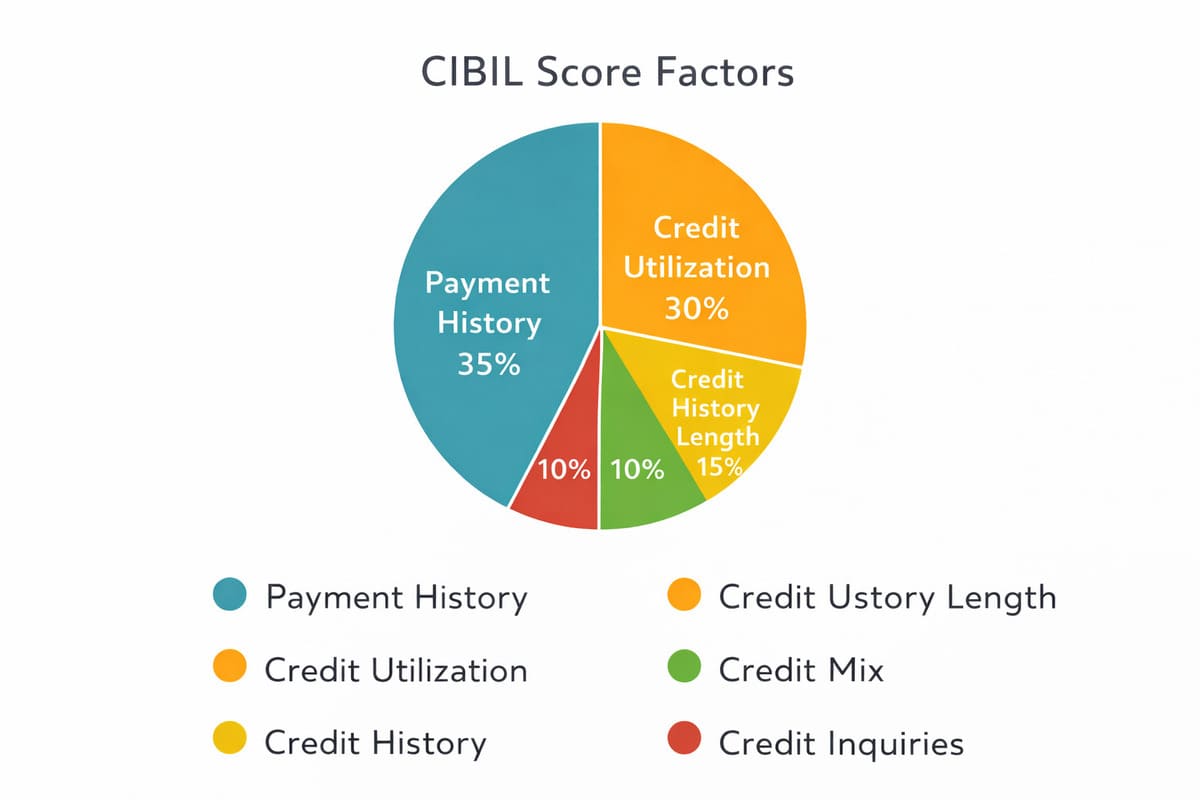

🔹 How Is CIBIL Score Calculated?

CIBIL calculates your score based on several factors:

1️⃣ Payment History (35%)

Paying EMIs and credit card bills on time has the biggest impact. Even one missed payment can reduce your score.

2️⃣Credit Utilisation Ratio (30%)

This is the percentage of credit you use from your total limit.

- Ideal usage: Below 30%

- High usage signals credit hunger and reduces your score.

3️⃣ Credit History Length (15%)

The longer your credit history, the better. Old accounts help build trust.

4️⃣ Credit Mix (10%)

A healthy mix of secured (home loan) and unsecured loans (credit cards) improves your score.

5️⃣ Credit Enquiries (10%)

Too many loan or credit card applications in a short time negatively affect your score.

Payment history and credit usage have the highest impact on your CIBIL score.

🔹 CIBIL Score Explained with Real-Life Example

To understand how a CIBIL score works, let’s look at a simple real-life scenario.

Example:

Rahul and Amit both apply for a personal loan of ₹5 lakh.

- Rahul’s CIBIL Score: 780

- Amit’s CIBIL Score: 620

What happens?

✔ Rahul:

- Loan approved quickly

- Gets lower interest rate (around 10–12%)

- Higher loan amount eligibility

❌ Amit:

- Loan may get rejected OR

- Gets higher interest rate (15–20%)

- Lower loan amount approved

📌 This clearly shows how your CIBIL score directly affects your financial life.

🔹 What Happens If You Have No CIBIL Score?

Many beginners or students have no credit history, which means no CIBIL score.

This is called “NA” or “NH” (No History).

Why is this a problem?

Banks cannot judge your credit behaviour, so:

- Loan approval becomes difficult

- Credit card applications may get rejected

How to Build CIBIL Score from Zero?

👉 Start with:

- Secured credit card (against FD)

- Small consumer loans (if needed)

- Buy now, pay later (use carefully)

📌 Use credit responsibly and your score will start building within 3–6 months.

🔹 Difference Between CIBIL Score and Credit Report

Many people think both are the same, but they are different.

CIBIL Score:

- A 3-digit number (300–900)

- Quick summary of your creditworthiness

Credit Report:

- Detailed report of:

- All loans

- Credit cards

- Payment history

- Defaults or delays

📌 Lenders check both before approving loans.

🔹 How to Check Your CIBIL Score for Free

You can check your score online easily.

Steps:

- Visit official CIBIL website

- Register with your details

- Verify using OTP

- View your score and report

📌 You are allowed 1 free report per year

👉 You can also check through:

- Bank apps

- Financial apps (like Paytm, Paisabazaar, etc.)

🔹 Smart Tips to Maintain a High CIBIL Score

Improving is one thing—but maintaining is equally important.

Follow these habits:

✔ Always pay full credit card bill (not minimum due)

✔ Keep credit utilization below 30%

✔ Avoid unnecessary loans

✔ Monitor your report regularly

✔ Keep a mix of credit types

📌 Small habits consistently followed = strong long-term score

🔹 CIBIL Score Myths You Should Ignore

Many people believe wrong information. Let’s clear some myths:

❌ Myth 1: Checking score reduces it

👉 Truth: Self-check is safe (soft enquiry)

❌ Myth 2: Closing loans improves score

👉 Truth: Properly closing loans helps, but old history is valuable

❌ Myth 3: High income = High CIBIL score

👉 Truth: Score depends on credit behaviour, not income

❌ Myth 4: One late payment doesn’t matter

👉 Truth: Even one missed EMI can impact your score

🔹 Common Reasons for Low CIBIL Score

Many people damage their score unknowingly. Common mistakes include:

- Missing EMI or credit card payments

- Paying only the minimum due

- Using too much credit limit

- Closing old credit cards

- Multiple loan enquiries

- Defaulting or settling loans

🔹 How to Improve CIBIL Score Fast (Proven Tips)

✅ 1. Pay All Dues on Time

Timely payments are the fastest way to improve your score.

Set auto-debit reminders to avoid missing due dates.

✅2. Reduce Credit Card Utilisation

If your limit is ₹1,00,000, try to keep usage below ₹30,000.

This alone can significantly improve your score within 2–3 months.

✅ 3. Avoid New Credit Applications

Every new application creates a hard enquiry.

Apply only when absolutely necessary.

✅ 4. Maintain Old Credit Accounts

Older credit cards improve your credit age. Avoid closing them unless required.

✅ 5. Check Your CIBIL Report for Errors

Sometimes wrong data affects your score.

- Incorrect loan status

- Duplicate accounts

- Wrong payment history

Dispute such errors directly on the CIBIL website.

✅ 6. Don’t Settle Loans (If Possible)

Loan settlement negatively affects your credit history. Always try to fully close loans.

✅ 7. Use Credit Responsibly

Having a credit card but using it wisely is better than having no credit history.

Simple habits can improve your CIBIL score over time.

🔹 How Long Does It Take to Improve CIBIL Score?

- Minor issues: 2–3 months

- Late payments: 3–6 months

- Defaults or settlements: 6–12 months

Consistency is the key. There are no instant shortcuts, but disciplined habits work.

🔹What Is a Good CIBIL Score for Loans?

- Home Loan: 750+

- Personal Loan: 700+

- Credit Card: 700+

Higher scores mean lower interest rates and better terms.

🔹 Final Thoughts

Your CIBIL score is not just a number—it is your financial reputation. Improving it requires discipline, patience, and smart credit behaviour. By paying on time, reducing credit usage, and avoiding unnecessary loans, you can steadily improve your score and unlock better financial opportunities.

Start today, stay consistent, and your future self will thank you.

”

🔹 CIBIL Score vs Other Credit Scores in India

Apart from CIBIL, there are other credit bureaus like:

- Experian

- Equifax

- CRIF High Mark

However, CIBIL is the most widely used by banks and NBFCs in India.

Frequently Asked Questions

Q1. What is a good CIBIL score in India?

Ans– A score of 750 or above is considered excellent.

Q2. Can I improve my CIBIL score in 30 days?

Ans-Minor improvements are possible, but major improvement takes 3–6 months.

Q3. Does checking CIBIL score reduce it?

Ans- No, checking your own score does not affect it

Q4. How many times can I check my CIBIL score for free?

Ans- You can check it once a year for free on the CIBIL website.

Q5. Is zero credit history bad?

Ans- Yes, lenders prefer some credit history over none.

Q6. What is the minimum CIBIL score for a personal loan?

Ans – Usually 700+, but some lenders accept 650+ with higher interest.

Q7. Can a low CIBIL score be fixed?

Ans – Yes, with timely payments and responsible credit use.

Q8. Does EMI bounce affect CIBIL score?

Ans – Yes, it negatively impacts your payment history.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Loan approval and interest rates depend on lender policies and individual credit profiles.

Shilpesh Rathod is the founder of All Finance Knowledge. He holds a B.Com degree along with JAIIB and CAIIB banking certifications, and brings 19+ years of experience in the banking sector across savings, investments, and financial planning. Read more: https://allfinanceknowledge.com/about-us/

4 thoughts on “CIBIL Score Explained: How to Improve It Fast”