Saving money regularly is one of the most important financial habits. However, where you invest your monthly savings matters more than how much you save.

In India, many people face a common confusion:

SIP vs RD – which option is better for long-term wealth creation?

Some prefer Recurring Deposits (RD) because they are safe and predictable. Others choose Systematic Investment Plans (SIP) for higher returns and long-term growth.

In this detailed guide, we will compare SIP and RD in simple language, with real-life examples, returns comparison, risks, taxation, and practical advice so you can make the right decision.

What Is SIP (Systematic Investment Plan)?

A Systematic Investment Plan (SIP) is a method of investing a fixed amount regularly—usually monthly—into mutual funds.

Instead of investing a large lump sum, SIP allows you to:

- Invest small amounts consistently

- Build financial discipline

- Reduce market timing risk

- Benefit from long-term growth

Key Features of SIP

- Start with as low as ₹500 per month

- Invests in equity, debt, or hybrid mutual funds

- Returns are market-linked

- Suitable for long-term goals

- Benefits from compounding and rupee cost averaging

Simple SIP Example

If you invest ₹5,000 per month in an equity mutual fund through SIP, your money is gradually invested in the stock market.

Over time, due to market growth and compounding, your investment can grow significantly.

What Is RD (Recurring Deposit)?

A Recurring Deposit (RD) is a traditional savings option offered by banks and post offices.

You deposit a fixed amount every month for a fixed period and earn guaranteed interest.

Key Features of RD

- Fixed monthly contribution

- Guaranteed returns

- Tenure from 6 months to 10 years

- Very low risk

- Suitable for conservative investors

Simple RD Example

If you invest ₹5,000 per month in an RD for 5 years at 6.5% interest:

- You know exactly how much you will receive at maturity

- There is no impact from market fluctuations

SIP vs RD: Basic Comparison Table

| Feature | SIP | RD |

| Type | Market-linked | Fixed income |

| Risk | Moderate to high | Very low |

| Returns | Variable (10–14% long term) | Fixed (5–7%) |

| Inflation protection | Yes | Limited |

| Best for | Wealth creation | Safe savings |

| Tax benefits | ELSS under 80C | Limited |

| Flexibility | High | Low |

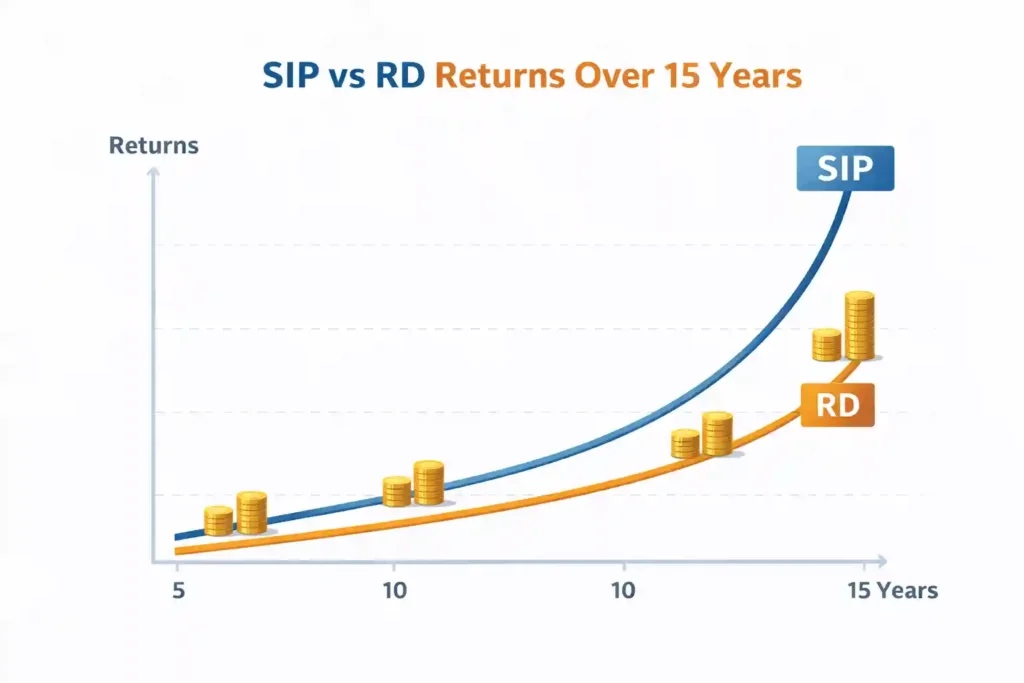

Returns Comparison: SIP vs RD (₹5,000 Per Month Example)

Returns Comparison: SIP vs RD (₹5,000 Monthly)

Let’s compare both options with a realistic example.

📊 Investment Assumptions

- Monthly Investment: ₹5,000

- Investment Period: 15 years

- SIP Return: 12% annually (assumed)

- RD Interest: 6.5% annually

🔹 SIP Returns

- Total Investment: ₹9,00,000

- Estimated Value: ₹25–30 lakh

🔹 RD Returns

- Total Investment: ₹9,00,000

- Maturity Value: ₹13–14 lakh

👉 Result: SIP clearly outperforms RD in the long term due to equity growth and compounding.

Why SIP Outperforms RD in the Long Run

1️⃣ Power of Compounding

SIP benefits from compounding, where:

- Returns generate additional returns

- Wealth grows exponentially over time

The longer you stay invested, the greater the impact.

2️⃣ Market Growth Advantage

SIP investments (especially in equity funds) grow with the economy and businesses.

RD, on the other hand, offers fixed returns that do not increase with economic growth.

3️⃣ Rupee Cost Averaging

SIP automatically buys:

- More units when prices are low

- Fewer units when prices are high

This reduces the overall cost of investment.

Risk Factor: SIP vs RD

Risk Factor: SIP vs RD

SIP Risk

- Market fluctuations can impact returns

- Short-term losses are possible

- No guaranteed returns

However, long-term investing (10–15 years) has historically reduced risk significantly.

RD Risk

- Almost zero risk

- Capital protection guaranteed

- Fixed returns

👉 Main drawback: Returns may not beat inflation.

Inflation Impact: The Hidden Factor

Inflation reduces the purchasing power of money over time.

Example:

- Inflation: 6%

- RD return: 6.5%

👉 Real return ≈ almost zero

This means your money is not actually growing in real terms.

SIP, especially in equity funds, has the potential to beat inflation and create real wealth.

Taxation: SIP vs RD

SIP Taxation

- Equity mutual funds are taxed as capital gains

- Long-term capital gains (LTCG) taxed at 12.5% above ₹1.25 lakh

- ELSS funds offer tax benefits under Section 80C

RD Taxation

- Interest is fully taxable

- Taxed as per your income slab

- TDS may apply

👉 SIP is generally more tax-efficient than RD for long-term investors.

Real-Life Example: SIP vs RD

Let’s consider a 30-year-old salaried person earning ₹40,000/month.

Option 1: RD

- Invests ₹5,000 monthly

- Safe but limited growth

Option 2: SIP

- Invests ₹5,000 monthly in an index fund

- Builds a much larger corpus over 15–20 years

👉 This shows why SIP is preferred for long-term financial goals.

Real-Life Example: SIP vs RD for a Salaried Indian

Consider a 30-year-old salaried professional earning ₹40,000 per month.

- Investing ₹5,000 in RD provides safety but limited growth.

- Investing ₹5,000 via SIP in an index fund can build a much larger retirement corpus over 15–20 years.

This is why SIP is often recommended for long-term goals, while RD is better for short-term stability.

Who Should Choose SIP?

SIP is ideal for:

- Young professionals

- Long-term investors (10–20 years)

- People aiming for wealth creation

- Investors comfortable with moderate risk

- Goals like retirement, education, or buying a home

Who Should Choose RD?

RD is suitable for:

- Conservative investors, not ready to take risks

- Short-term goals with safety

- Emergency funds

- People who cannot tolerate market volatility

- Senior citizens (as part of safe allocation)

SIP vs RD for Beginners: Which Is Better?

If you are a beginner:

👉 Start with SIP in:

- Index funds

- Large-cap mutual funds

👉 Invest small amounts and increase gradually.

If you want complete safety and predictable returns, RD is fine. But if your goal is long-term wealth creation, SIP is the better choice.

Can You Invest in Both SIP and RD?

Yes—and this is actually the best strategy.

Balanced Approach:

- SIP → Long-term growth

- RD → Short-term stability

This combination gives you:

✔ Growth

✔ Safety

✔ Flexibility

Common Mistakes to Avoid

❌ Choosing RD only due to fear

❌ Expecting quick returns from SIP

❌ Stopping SIP during market fall

❌ Not considering inflation

❌ Investing without clear goals

Final Verdict: SIP vs RD – Which Is Better in the Long Term?

Choose SIP if you want:

- Long-term wealth creation

- Higher returns

- Inflation protection

✔ Choose RD if you want:

- Safety

- Guaranteed returns

- Short-term savings

👉 For long-term wealth creation, SIP is clearly the better choice.

For better understanding, one can read our article on how to plan a monthly budget on a ₹30,000 salary

Frequently Asked Questions (FAQs)

Q1. Is SIP better than RD for long-term investment?

Ans- Yes, SIP generally provides higher returns due to compounding and market growth.

Q2-Can SIP give negative returns?

Ans- Yes, in the short term. But long-term investments have historically shown positive results.

Q3-Is RD safer than SIP?

Ans-Yes, RD is safer as it offers guaranteed returns.

Q4-Can I stop SIP anytime?

Ans- Yes, SIP is flexible and can be paused or stopped anytime.

Q5-What is the minimum amount for SIP and RD?

Ans-Yes, SIP is flexible and can be paused or stopped anytime.

Final Thoughts

Both SIP and RD have their place in financial planning. The right choice depends on your goals, risk tolerance, and investment horizon.

However, if your aim is to build real wealth over time, SIP stands out as the more powerful option.

The key is simple:

👉 Start early

👉 Stay consistent

👉 Think long term

DISCLAIMER

This article is for educational purposes only and does not constitute financial advice. Please consult a qualified financial advisor before making investment decisions.

About the Author

Shilpesh Rathod writes about personal finance, mutual funds, and beginner investing in India. His goal is to simplify money concepts and help readers make informed financial decisions.

7 thoughts on “SIP vs RD: Which Is Better for Long-Term Wealth in India?”